The Great Mile High Real Estate Investors Summit has partnered with Realty411, BRRRR Loans, Invest Success and Realty Investors Group to present the premiere Colorado-based Great Mile High REI Summit in Denver to be held on March 8 – 10, 2024. The Great Mile High Real Estate Investors Summit is not your ordinary real estate event. This multi-day REI extravaganza will host 30 speakers at the unique Curtis Hotel in downtown Denver. Enjoy educational and networking opportunities, happy hours, lunches, dinners, entertainment, and a property bus tour around Denver. Stay to hit the slopes and enjoy all that beautiful Colorado has to offer.

article continues after advertisement

There is an early-bird discount for readers and friends of Realty411 and REI Wealth magazines. To celebrate Realty411’s most recent Investor Summit held in Irvine, California last week, we have put together a special code of IRVINE100OFF for a discounted admission rate for Denver’s Summit. Be sure to use IRVINE100OFF at checkout for $100 off your summit ticket purchase.

A limited number of discounted hotel rooms at The Curtis Hotel Downtown Denver are available at a special rate of $179 per night. The regular rate for that weekend is from $200 to $300 per night. Be sure to act now before the room block is full.

For companies or individuals who would like to inquire about speaking opportunities, please contact, [email protected]. See you in Denver this March for this life-changing summit with some of the nation’s top educators in real estate.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/The-Great-Mile-High-Real-Estate-Investors-Summit.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-21 02:58:062023-08-22 01:18:01Learn About The Great Mile High Real Estate Investors Summit

Life, with all its twists and turns, grants us moments of joy and success, yet it also challenges us with uncertainties. As we journey through the tapestry of time, it’s vital to be equipped with the tools that safeguard our hard-earned assets and ensure our wishes are honored. Welcome to the realm of estate planning – a treasure trove of wisdom that empowers you to craft a secure future for yourself and your loved ones.

article continues after advertisement

1. The Best Estate Planning Tip: Seize the Present Moment

In the symphony of life, procrastination is your foe. The greatest estate planning advice is to initiate the process now, while clarity and competence are your companions. Forge your plan for asset management and care in the face of adversity. Be the architect of your destiny, steering clear of court interference.

2. Beyond the Will: Embrace the Living Trust

A will, though essential, can lead to probate – a journey through courts that consumes time and money. Step into the embrace of a Living Trust, a sanctuary that shields your estate from probate’s grasp. For those with real estate and substantial assets, this is your golden ticket.

3. Fund Your Trust: Empower Your Legacy

Empower your Living Trust by aligning all your assets with its name. A simple signature card at the bank, overseen by your Powers of Attorney, is your key to unifying your financial fortress.

4. Safeguarding the Wisdom: Storing Important Papers

Preserve your precious documents within the embrace of fireproof protection. Ensure your Powers of Attorney hold a key to your safe box, ensuring that your plans remain secure.

5. A Guardian of Your Health: Health Care Proxy

Life’s journey can present incapacitation. Who will speak for you then? A health care proxy designates a trusted representative to make critical medical decisions on your behalf. Protect your healthcare wishes and share them with your physician through a healthcare Power of Attorney.

article continues after advertisement

6. Alternates for Assurance: Naming Agents Wisely

Fortify your estate plan by naming alternate agents to represent your interests. Be the architect of your fate, ensuring your choices are honored even if your first option is unavailable.

7. An Evolving Masterpiece: Update Your Estate Plan

As seasons change, so does life. Keep your plan aligned with your reality, adapting to personal shifts, economic tides, and tax laws. Stay current and let your legacy shine.

8. Armor Against Creditors: Trusts for Protection

Shield your assets from the clutches of creditors. Trusts, designed with protective provisions, offer an impenetrable sanctuary for your wealth, safeguarding your legacy for generations to come.

9. Homestead Haven: Protecting Your Home

The fortress of your home can be fortified further. Secure your residence with the powerful shield of the homestead, offering protection against creditors up to a significant amount.

10. Gifts of Abundance: Reducing Taxes

Bestow gifts to your loved ones with a generous heart, for gifts between spouses are a tax-free expression of love. Harness the art of gifting to reduce the size of your estate, potentially easing the burden of estate taxes.

Dodge probate, but remember, it’s not the same as evading estate taxes. Consult an estate planning expert to unravel the intricate web of taxation, ensuring your legacy remains untarnished.

12. Destiny in Designation: Beneficiary Forms Matter

Wills and Trusts are the symphonies, but beneficiary designation forms are the conductors. Ensure your orchestra performs harmoniously by keeping these forms accurate and up-to-date, guiding your assets to their rightful heirs.

Embrace the secrets of estate planning, unlocking the doors to financial security and serenity. Paint your legacy with colors of abundance, knowing that your journey through life will be woven into an enduring masterpiece. Let your story inspire others to sculpt their futures, fortified by the wisdom of estate planning.

Schedule a Free Financial Fitness Strategy Session with Kris Miller, LDA

30+ years of experience assisting others in growing & protecting their wealth. Helped more than 6,000 families avoid financial disaster by strategically planning for their futures. Not one person has lost a single dime on her watch. Her clients learn how to change their families’ financial realities and create incomes they will never outlive

Healthy Money Happy Life Make an Appointment with Kris

CA Insurance License OC25427 I am not an attorney. I can only provide self-help services at your specific direction. Should you need legal advice, you will need to consult an attorney. We do Estate Planning, Wills, Living Trusts, Power of Attorney, Health Care Directives and Deeds. Legal Document Assistant in Riverside County, California LDA #000041 Riverside County, expiring 10/15/2021

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/unlock.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-16 03:14:222023-08-16 03:14:26Unlocking the 12 Secrets of Estate Planning: Building a Legacy of Financial Freedom and Protection

Buying rental property is a great way to invest for the future. Just watch out for these common tricks that sellers use to inflate the appraised value.

Be careful when buying rental property. We stayed at a motel for a week one winter. The bill showed twice what it should have, but since I already paid the correct amount in cash, I thought nothing of it. When we noticed that the lobby and swimming pool were unheated, we thought it was frugality. Only a year later, when I read a news story about a new owner struggling to make the motel work, did I realize what was going on.

article continues after advertisement

The owner had been planning to sell. To prepare, she was using the two most basic ways to inflate the appraised value: decrease expenses and increase reported income. By stopping repairs and quietly adding $100 in income every day, she may have shown $45,000 more net income for the year. At a .08 capitalization rate, that means the appraisal would come in $562,000 higher than it should have. Oops! The poor guy who overpaid!

Do you want to avoid a mistake like that when buying a rental property? You need to watch for tricks like these. You also have to understand the basics of appraising income property.

It starts with the capitalization rate, or “cap rate.” If investors in an area expect a return of 8% on assets, the cap rate is .08. Net income before debt service is divided by this to arrive at the value of a property. I explain this further in another article, but the primary point here is to remember that every dollar of extra income shown will increase the appraised value by $12.50 with a cap rate of .08, or by $10, if the cap rate is .10.

Sellers Dirty Tricks

If sellers of rental properties increase the net by honest means, then the property should sell for more. Unfortunately, there are many dishonest ways, both legal and fraudulent, that are sometimes used. Unlike sellers of houses, who may cover foundation cracks with plaster, the tricks used by sellers of income properties aren’t about appearance. They are about income and expenses.

Income can be inflated by showing you the “pro forma,” or projected income, instead of the actual rents collected. Ask for the actual figures, and check to see that none of the apartments listed as occupied are actually vacant. Also, be sure that none of the income is from one time events, like the sale of something.

article continues after advertisement

Income from vending machines is a gray area. Smart investors subtract this from the net income before applying the cap rate, then add back the value of the machines themselves. If laundry machines make $6,000, for example, that would add $75,000 to the appraised value (.08 cap rate), if included. Since they are easily replaceable, adding the $10,000 replacement cost instead makes more sense.

Hiding expenses is the most common of seller’s tricks. Paying for repairs off the books, or just avoiding necessary repairs for a year, can dramatically increase the net income. Demand an accounting of all expenditures. If a number in an expense category is suspicious, replace it with your own best guess.

Analyze each of the following, verifying the figures as much as possible, and substituting your own guesses if they are too suspect: vacancy rates, advertising, cleaning, maintenance, repairs, management fees, supplies, taxes, insurance, utilities, commissions, legal fees, and any other expenses. This is how you make buying rental property safe.

Joe Arias and his partners have flipped hundreds of properties in the Southern California Region. He has developed cutting-edge systems to simplify and scale the entire remodel process that can easily be applied to flipping, rentals, wholesaling, and other passive income strategies. More recently, Joe founded a real estate investing education company called RealSuccess Investments, allowing him to share his tools and systems with hundreds of up-and-coming investors.

RealSuccess is focused on education on flipping, rentals, passive income, and wholesaling.

Joe is also a best-selling author. He has written 4 books: Finding your RealSuccess, First Steps to Flipping, R stands for Rentals and Retirement, and Wholesaling Real Estate.

“I came from Argentina when I was 20, I am 40 years old now. I didn’t know anyone, I am CERO generation, usually people say, I am first or second generation but I was the one that crossed the border, no language, no friends, no family, no money, nothing, nada… If I can do it, anyone can.”

From a young latino immigrant to a celebrated real estate investor, Joe is a true testament to hard work and discipline. As an investor, he has made it his mission to help others achieve financial freedom while enjoying living a life of passion, fulfillment, and empowerment.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

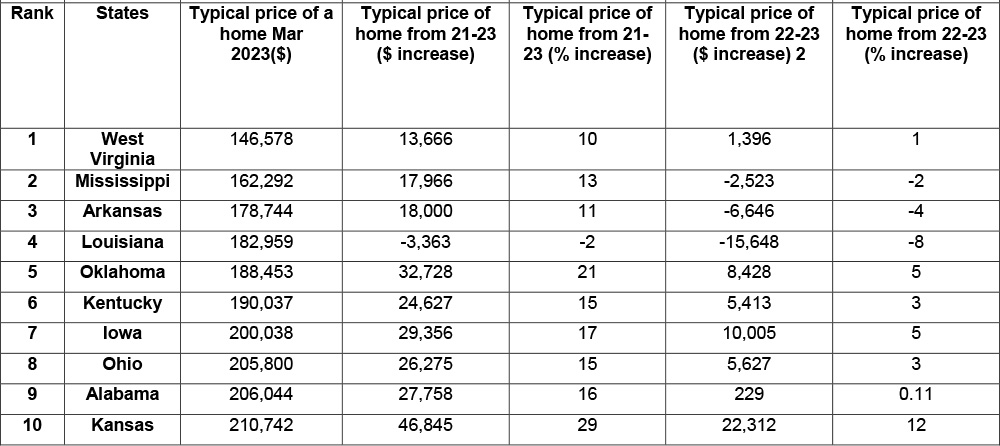

West Virginia is the least expensive state to own a home, with a typical house price of $146,578 as of March 2023.

article continues after advertisement

Mississippi, Arkansas, Louisiana, and Oklahoma round out the top five.

The study analyzed the typical cost of homes in America, as well as percentage and price increases from 2021 to 2023.

New data has revealed the cheapest states to own a home in America.

The research, conducted by real estate experts Agent Advice, analyzed the typical price of homes throughout the country from March 2021-March 2023. The data also considered price and percentage increases to supply a comprehensive account of real estate in America.

West Virginia takes the crown as the least expensive state to own a home. The research found that typical house prices were $146,578 as of March 2023, 57% less than the national average ($338,649). The typical price increased by 10% and $13,666 from March 2021, the second-lowest monetary increase in the United States, with a 1% and $1,396 rise between March 2022-March 2023.

Mississippi receives a silver medal as the second cheapest state to own a home. In the Magnolia State, a typical house price was $162,292 as of March 2023, 52% below the national average. The Southeastern state also has the third lowest monetary increase in house prices, with a $17,966 and 12% rise between March 2021-March 2023. However, typical house prices depreciated by 2% and $2,523 from March 2022-March 2023, showing a slight decrease in the last two years.

Arkansas ranks in third place. In the Natural State, typical house prices were $178,744 as of March 2023, 47% below the national average. The typical cost rose by 11% and $18,000 between March 2021-March 2023, standing for the fourth lowest monetary increase. The research also reveals typical prices decreased by 4% from March 2022-March 2023, saving house hunters an extra $6,646.

article continues after advertisement

Louisiana is the fourth cheapest state to own a home in America, with typical house prices being $182,959 as of March 2023, 46% less than the national average. The Pelican State stands for the highest reduction, rather than an increase in prices throughout America, with house prices falling by 2% and $3,363 between March 2021-March 2023, with an 8% and $15,648 reduction between March 2022-2023.

Oklahoma comes in fifth place. The research shows that typical home prices were $188,453 as of March 2023, 44% below the national average. This is 21% more than the typical house price reported as of March 2021, with a 5% and $8,428 monetary rise within the last two years.

Kentucky ranks in sixth place. The data has benchmarked typical house prices at $190,037 as of March 2023, 44% below the national average. Overall, property values increased by 3% and $5,413 from March 2022, and 15% and $24,627 from March 2021, the seventh-lowest monetary rise in the country.

Iowa is the seventh cheapest state to own a home, with typical house prices reported as $200,038 in March 2023, 41% below the national average. The Hawkeye State has experienced a 17% and $29,356 increase in property values between March 2021-March 2023, with 5% and $10,005 accounting for March 2022-March 2023.

Ohio, with a typical home value of $205,800 as of March 2023, is the eighth cheapest state to own a home. Alabama follows in ninth place with a typical price of $206,044, while Kansas rounds out the top ten at $210,742.

Chris Heller, Co-founder of Agent Advice, has commented on the findings: “The U.S. housing market is estimated to be worth $43.4 trillion in 2023. To take advantage of this, consumers and agents alike must understand the ever-changing nature of the real estate market.”

“Overall, there has been an increase in cost in the last three years throughout the nation. However, this research shows that there has also been a depreciation in multiple states over the last two years, showing a rise in more affordable housing.

“In Louisiana, for example, typical house prices have reduced by 8% and $15,648 within the last two years. So, it will be interesting to see if this trend in the cost of housing will eventually decrease throughout the country.”

The top ten cheapest states to own a home in America

Agent Advice is a team of real estate experts providing hand-selected recommendations to help real estate businesses grow.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/house-on-US-map.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-11 03:28:522023-08-11 03:28:56New Data Reveals the Top Ten Cheapest States to Own a Home in America

Our guest will be Adiel Gorel with ICG Real Estate Investments.

ABOUT MR. ADIEL GOREL – CEO of International Capital Group – Keynote Speaker

Adiel Gorel is the CEO of ICG, a prominent real estate investment firm located in the San Francisco Bay Area. Since 1983 he has successfully been assisting thousands of investors with purchasing U.S. properties.

Through ICG he has personally invested in hundreds of properties for his own portfolio and was involved in the purchase of over 10,000 properties for ICG’s investors in Phoenix, Las Vegas, Orlando, Tampa, Jacksonville, Dallas, Houston, Austin, San Antonio, Atlanta, Nashville, Huntsville, Boise, Oklahoma City, Tulsa, Salt Lake City, to name just a few.

Mr. Gorel holds a master’s degree from Stanford University. His professional experience includes Management and Director Positions in firms including Hewlett- Packard, Excel Telecommunications, and biotechnology firms.

Join Us for an In-Person Event in Irvine, CA- LEARN FROM SOPHISTICATED INVESTORS

Be sure to join us IN PERSON. We will have wonderful resources, plus guests will have access to private capital, plus business and commercial funding as well. We have investors joining us from across the nation for one day of networking.

Our educators will be providing valuable insight, including: Kaaren Hall, uDirect IRA Services, LLC Hector Padilla, HP Capital Investments Christopher Meza, Real Titan Acquisitions Paul Finck, The Maverick Millionaire Rusty Tweed, TFS Properties Barry Duron, AltLender Mortgage Jeremy Rubin, The Friendly Flipper Kris Miller, Legacy Wealth Strategies Deborah Razo, Women’s Real Estate Network Julie Harrison, Buy Direct Mississippi Emily Nesselroad, 3 Fives Properties Paul Wilkins, Approved Inheritance Cash Jim Edenfield, Invest Success Tim Emery, The Great Mile High Real Estate Investors Summit AND MANY MORE!

Now is the moment to grasp this opportunity — the chance to network with sophisticated investors from California and around the country. Join us for our special REI conference.

Be sure to pencil this date now and join us in-person to gain specialized insight and knowledge. The information shared on this day could catapult your portfolio to new levels. Discover our new property portal, our VIP perks, plus connect with new and past industry resources.

Advertisements:

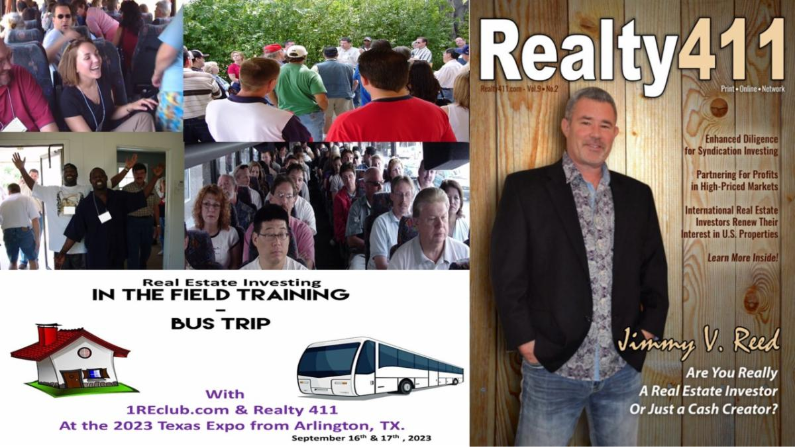

– Join Us for Realty411’s Lone Star Wealth Summit –

Are you ready to grow your real estate portfolio to new levels of abundance? If so, be sure to join us for Realty411’s new Lone Star Wealth Summit.

Investors, Realty411 is hosting a Real Estate WEALTH Summit & In Field Bus Training in Arlington, Texas on September 16th & 17th.

Enjoy a day of learning and networking. Our educators include:*

* Chander Mishra MD MBA CPE FASE FASA FAACD – Blue Ocean Capital * Bob Bluhm, Esq — Asset Protection Attorney & Public Speaker * Joseph Kimbrough- Apex Real Estate Investments * Brian Carlson – Subject-To Real Estate Academy * Joseph V. Scorese – BRRR Loans * Brad Blazar – Capital School * Steve Davis – Total Wealth Academy * Jimmy Reed – 1REclub.com * Jonah Dew – The Money Multiplier * Jim Edenfield – Invest Success * Tim Emery – Great Mile High Investor Summit * Arnie Abramason — Texas Tax Sales * Joel M. Desilets – Damascus Partners, LLC * Paul Finck, The Maverick Millionaire ® * AND MANY MORE!

This is our first Lone Star Wealth Summit with the Bus training since 2018. Make sure to register now for both events in Arlington, TX.

The Wealth Summit is on Saturday September 16th in Arlington, TX. The link below will help you register and learn more about the Guest Speakers and Schedule of events.

Register now and you get in the Expo for FREE. However, tickets are limited and will not last. Be sure to read information about the In- Field Bus Tour on Sunday, September 17th.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/Adiel.jpg3661000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-10 07:18:482023-08-10 07:18:53Attention: It’s time for another educational and exciting Realty411 Virtual Investing class!

Realty411 invites you to gain the latest insight on real estate investing. Join us in Southern California to learn the latest techniques to increase your existing rental portfolio.

New investors, discover how easy it is to begin one here.

Experienced educators and top leaders in the industry are ready and excited to teach our guests. Join us for an amazing day of learning and networking.

It’s National Homeownership Month: Chase Debuts Updated Offerings andReveals First-Time Homebuyer Attitudes Study

Amid Economic Fluctuations, 70% Of First-Time Buyers Still See Homeownership As An Important Step To Building Wealth

Chase Home Lending unveiled a refreshed suite of homebuyer resources and findings from a recent consumer survey. Chase’s new homebuyer product offerings, educational resources, and easy-to-use tools have been designed to help consumers navigate the homebuying process and manage homeownership.

Despite the fluctuating housing market this past year, Chase’s latest First-Time Homebuyer Study revealed that confidence levels remain high with 44% of respondents indicating they are confident they’ll be financially ready to purchase in the coming year, up 12% YoY.

Refreshed Suite of Chase Offerings and Educational Resources

article continues after advertisement

Chase has expanded its portfolio of resources to support customers on their path to homeownership. New and updated resources include:

Lock and Shop: Chase’s new Lock and Shop offering allows you to lock in your mortgage rate for 90-days with

no upfront fee when using Chase Homebuyer Advantage.

Locking in a rate helps customers move quickly and gives them peace of

mind while shopping around for a home. Customers must find their

property within 60 days, and will have the option of a one-time float

down if rates improve. Once a customer finds their

home, they’ll also have the added confidence of Chase’s Closing Guarantee,

which guarantees an on-time closing in as little as 21 days, or the customer will receive $5,000.

Beginner To Buyer Season II Now Available: Chase recently launched the second season of its award-winning homebuyer education podcast.

Beginner To Buyer

offers 10 new episodes featuring conversations

with real buyers and expert guests discussing homebuying and ownership,

home equity, common misconceptions, renovations, and investment

properties. Buyers can dive deeper into these topics and more in Chase’s

Homebuyer Education Center.

Savings + Assistance Programs: Finding homebuyer grants and assistance programs is now quick and easy with Chase’s

Homebuyer Assistance Finder.

Users can search and discover

grants and programs they may qualify for, like Chase’s $5,000 grant for

eligible homebuyers purchasing in majority-Black and Hispanic

neighborhoods throughout the U.S.

$200 Pilot Program:Prospective buyers with an active loan offer from another lender can

compare their offer to Chase’s with a home lending advisor. Chase will

give eligible buyers $200 if they can’t match the offer or do better.

The

benefit is currently available for Chase customers

in Houston, Ohio, and Arizona.

“The homebuying process can be complex, so it’s critical that homebuyers have the right knowledge, tools and experts to help them,” said Sean Grzebin, Head of Consumer Originations, Chase Home Lending. “The latest set of resources from Chase, coupled with our network of home lending advisors, were designed with the current needs of homebuyers in mind, like locking in a rate and finding opportunities for savings. We’re excited for consumers to explore our updated offerings and engage with tools that can help them achieve homeownership.”

New Research From Chase

The study was commissioned to better understand the needs of first-time homebuyers purchasing amid an uncertain economic environment. Homebuying attitudes, behaviors, and expectations were evaluated, specifically as it relates to confidence, financial readiness, and more. Though the current state of the economy has a considerable impact, 58% of respondents said that they were likely to purchase in the next 12 months, and 70% still see homeownership as an important step to building wealth.

article continues after advertisement

“Prospective homebuyers are eager to tap into the wealth-building capabilities that homeownership brings,” shared Grzebin. “Despite market uncertainty and lengthened timelines, first-time buyers are making the necessary lifestyle adjustments to reach their homeownership goals.”

Respondents know what they need to do to get financially ready for homeownership, and confidence in their financial readiness is improving (up 12% YoY). Two-in-three respondents have improved their credit score and implemented budgeting techniques to save more for a home. Sixty-four percent are working to improve their credit score, 63% are creating and sticking to monthly budgets, and 67% are making lifestyle adjustments.

The study is based on the responses of 1,900 U.S.-based consumers fielded in Q4 2022 amongst those who have never owned a home. For more information about Chase Home Lending, visit www.chase.com/mortgage.

Additional survey findings:

Black Americans represent 21% of first-time homebuyers in 2022.

Thirteen percent of first-time homebuyers are Hispanic.

Single women make up 22% of first-time homebuyers.

First-time homebuyers are more likely to be married or partnered Millennials

(56%), but nearly 40% are single. Twenty-five percent are Gen X, and even some

(7%) Boomers are entering the homebuying process for the first time.

One-in-four first-time homebuyers moved in with their parents/family as a money-saving strategy, up

12% YoY.Two-in-five future homeowners plan to move in with family, up from

one-in-five last year. Even Gen X is more likely to resort to live with family than a year ago, with

19% having already moved in (up from 10% in 2021), and an additional

14% (up from 7% in 2021) expecting to do so.

Sixty-three percent know the financial-related changes and activities they need to do to qualify for a loan.

Fifty-nine percent know how much money they need to have to purchase a home, yet

46% are not sure they will ever be able to save enough.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/save-money-to-buy-a-house.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-09 05:03:332023-08-09 05:03:38Saving Up To Buy A Home—Would You Consider Moving In With Family? Some Buyers Are

The 2023 year continues to be one of the most interesting, perplexing, and challenging years that many of us have ever seen. From my perspective, there has never been a year like this year to compare it to as it relates specifically to housing, finance, investments, insurance, and to our federal government.

The only constant in life is change. Remember, if you always do what you’ve always done, you will always get what you’ve always gotten. As such, please be flexible and ever-changing as needed to minimize your downside risks and to maximize your financial gains.

Let’s take a look next at my Top 10 topic points that I will be sharing and discussing with my So-Cal Real Estate Investors group this month:

article continues after advertisement

1. Credit downgrades for the US, Fannie Mae, and Freddie Mac:

The Fitch credit rating agency just downgraded our federal government and the two largest secondary market investors for 70% of all mortgages named Fannie Mae and Freddie Mac, which have both been under government control since the fall of 2008 when they both almost imploded. The new credit rating is AA+ for all three entities after falling from the highest AAA credit rating.

As a result, the borrowing costs will likely increase while moving mortgage rates higher along with the 10-year Treasury yield which is inverse to the 10-year Treasury bond price like a seesaw. All 30-year fixed mortgage rates are tied to the 10-year Treasury yield directions, not to the fed funds rate which affects other consumer debts like credit cards, school loans, and car loans. Don’t be surprised if we soon see double-digit mortgage rates above 10%. The all-time record high 30-year fixed mortgage rate reached 18.6% in October 1981, by comparison.

Both Fannie Mae and Freddie Mac are highly leveraged with derivatives (a complex financial and insurance hybrid instrument) which can cause them to default on their investments due to triggering factors like rising distressed mortgage or foreclosure rates. If so, they may be forced to sell off some of their tens of millions of mortgages held in their portfolio to deep-pocketed corporations like BlackRock, Vanguard (largest BlackRock shareholder), and Blackstone (a BlackRock spinoff that’s also the world’s largest commercial real estate owner).

2. Why did mortgage rates reach all-time record lows in recent years?

Answer: The Federal Reserve created the Quantitative Easing (QE) program in November 2008 shortly after the US and global financial markets almost collapsed on September 29, 2008. The QE program is a fancy name for creating money out of thin air to buy stocks, bonds, and mortgages so that asset values don’t fall.

Back in 1961, President John F. Kennedy helped back the Operation Twist monetary policy program in an attempt to drive down long-term interest rates while buying and selling gold and gold-backed dollars at the same time. The “twist” name was partly derived from the Chubby Checker Twist dance craze.

In 2011, Operation Twist was brought back on a larger scale as both short-term and long-term bonds were simultaneously purchased and sold to artificially suppress the 10-year Treasury yield while driving the 30-year mortgage rate down to as low as the 2% rate ranges to boost home sales and prices. In recent years, the Federal Reserve became a net seller of assets purchased through Quantitative Easing. Due to fewer buyers for our debt, the lowered demand pushes the price down while boosting the 10-year Treasury yield. When bond prices fall, yields and corresponding 30-year fixed mortgage rates and borrowing costs rise.

The Fed’s record-setting rate hikes makes the borrowing costs for the US Treasury much higher as well. We’re on pace for $1 trillion dollars per year in interest payments made on the all-time record federal debt.

3. Insurance costs continue to skyrocket:

About 22% of homeowner insurance companies have completely stopped offering homeowners insurance here in California. As shared before, more than 70% of residential properties in California have a mortgage that requires active homeowners or landlord insurance. If not, it can trigger a foreclosure filing because the lender or mortgage loan servicing company requires homeowners insurance that lists them as a “named insured” in the event of a fire, flood, or some other type of property damage.

State Farm, Farmers, AIG, Chubb Geico, and others are just some of the insurance companies that have decreased or completely eliminated the issuing of new or renewal policies in California, Florida, and elsewhere. The reinsurance market is freezing up for insurance carriers, which is somewhat akin to their version of Fannie Mae, Freddie Mac, or secondary market derivatives investors who replenish capital for banks or insurance companies.

Due to fewer investors for riskier insurance in the reinsurance marketplace and fewer insurance companies willing to write new policies, the prices charged for new borrowers has absolutely skyrocketed. For example, a homeowner in St. Augustine, Florida (America’s first city) saw her annual insurance premiums for her 120-year old home rise from $8,800 to $36,000.

4. Housing and mortgage trends nationwide:

There are 140 million housing units in America.

64.8% of homes have a mortgage (96,320,000).

31.2% of homes have no mortgage (43,680,000).

There are almost one million Airbnb and VRBO rental units.

There are currently 1.7 million housing units in America under construction.

There are 44 million rental units across the nation.

80% of retirees own a home while almost half live near poverty.

Retirees (Baby Boomers and older Generation X) own 55.58% of the nation’s housing stock (55.8% of 140 million housing units = 77,812,000; 44% of these units have a mortgage or 34,237,280 properties). If half of these property owners are in distress, this could equal 17,118,640 properties, which might be equal to almost 39% of the rental market.

The IRS continues to remove family transfer benefits by way of trusts and other entities that may rapidly increase the amount of capital gains taxes which the heirs of older American property owners must pay following death. If so, it may accelerate the number of future listings so that heirs can pay their higher taxes.

5. Homeowner bailout options:

Forbearance agreements: The lender agrees to postpone or delay their foreclosure actions with the delinquent borrower. Sometimes, these foreclosure postponements may last months or years.

Deferment: The lender agrees with the borrower’s request to delay or defer their delinquent payments until a later date. In some cases, the late payments and penalties are added years later when the loan may become all due and payable.

Loan modification: The lender or mortgage loan service company agrees to reduce the existing interest rate and/or monthly payment amount so that the mortgage is more affordable as a way to avoid foreclosure.

Loan repayment plan: Both the lender and borrower mutually agree to add unpaid delinquent payments and late fees to the existing mortgage which may slightly increase their monthly payments or increase the loan term to give the borrower more time.

Reinstatement: After the borrower and lender agree to modify the monthly payments to avoid foreclosure, the loan is removed from foreclosure status and reinstated in “good standing.”

Seller-financed sales: If the homeowner needs a quick sale to a new buyer who can effectively take over his monthly mortgage payments and give the seller some much needed cash, the seller may consider creating some type of wraparound mortgage {contract for deed or all-inclusive trust deed (AITD)} or “subject-to” property transfer in which the buyer receives the deed to the property that is “subject-to” the existing mortgage still secured by the property.

Short sale: If and when the mortgage debt is greater than the current market value for the property (aka “upside-down” mortgage), the homeowner may consider contacting an experienced local Realtor who can help negotiate a discounted mortgage payoff with the lender when they find a qualified new buyer.

“Cash for Keys”: During the depths of the last major national foreclosure crisis between 2009 and 2013 especially, lenders were offering delinquent homeowners upwards of several thousand to $25,000 + to vacate the home while not damaging it or removing appliances.

Bankruptcy: For homeowners who are days away from losing their home at the final lender auction sale, they may consider filing Chapter 7 (complete liquidation of most debts) or Chapter 13 bankruptcy (a longer term workout payment plan).

6. The collapsing automobile lending sector: There are now 20,000 car repossessions per day and 600,000 repos per month.

Car insurance has increased almost 20% over the past year.

In 2019, the average car payment was near $350 – $375. Today, it’s closer to $730 per month. Yes, car payments have doubled in just four years as the purchasing power of the dollar rapidly declines.

The average cost of full coverage car insurance in Florida is now $300 per month. In 2021, Florida averaged more than 1,100 car accidents per day with 449 of these accidents involving alleged injuries which is a major factor for skyrocketing insurance costs there and elsewhere.

85% of new cars are financed with upwards of 125% loan-to-value (LTV) being fairly common partly to cover taxes, tags, warranties, and other costs.

1-in-6 Americans pay more than $1,000 per month for car payments. After adding insurance ($200 to $300+), gasoline ($200 – $300+), oil changes, and other maintenance expenses to the monthly payment, many people are paying upwards of 20% to 40%+ of their gross monthly income just for their car while paying another 40% to 50%+ per month for housing. (Partial source: First Notebook)

The choice between paying a mortgage or rent payment and making a car payment on time becomes more challenging as the economy continues to weaken.

7. Commercial real estate trends:

Multifamily apartment buildings have fallen the most out of all commercial property asset classes with a -13.8% year-over-year price drop as of May 2023. This is almost double the annual percentage losses for office buildings.

Right now, we’ve never had more residential housing units under construction at the same time with upwards of 1.7 million units, which includes a high percentage of new apartment units. The wave of new housing units that later hit the market for sale or lease may drive down sales and rental prices for other nearby properties.

Approximately 22% of all commercial mortgages nationwide were non-recourse loans as of 2021, per the Federal Reserve. A “non-recourse” loan makes it easier for the borrower to walk away and avoid deficiency judgments.

article continues after advertisement

8. Estimated U.S. Cost of Living:

Food – $1,000 per month Car Payment – $716 per month Car Insurance – $150 per month Gas – $200 per month Cell phone – $100 per month Housing – $1,702 (average one-bedroom apartment rent) Health or Medical Insurance – $500 per month Utilities and Internet – $150 per month (it’s closer to $500/month in CA) Student Loans – $300 (monthly payment is 40% below national average) Credit Cards – $300 (monthly payment is 40% below national average) —————————– Total: $5,118 per month Annual: $61,416

Median Individual Gross Income: $34,987 Median Individual Gross Losses (taxes not included): – $26,429 (negative) Median Household Income: $80,440 (two or more income sources)

How to set aside money each year: If you break down $10,000 into a daily savings goal, you would need to save about $27 per day to reach $10,000 in one year. To save $20,000 per year, reduce your monthly expenses by $54 per day.

9. Credit card debt:

Unpaid credit card debt recently surpassed $1 trillion for the first time ever and rates and fees reached all-time record highs this year.

“A credit card borrower with the average $5,733 credit card balance at 20.55% will be in debt for over 17 years if they make just the minimum payments every month, according to Rossman. They will also pay about $8,400 in interest on top of the $5,733 balance, he said.” – CNBC

Sadly, a higher percentage of credit card rates today are closer to 25% to 30%+, so it will take much longer to pay the debt off.

Paying off credit card debt: 1. Opt for zero percent balance transfers; 2. Create a debt payoff plan; 3. Seek professional help; 4. Keep saving, if possible; and 5. Consider filing for bankruptcy protection (as low as $200 online for do-it-yourself plans). If so, I will teach you how to quickly rebuild your credit after the Chapter 7 bankruptcy discharge.

10. Finding distressed properties:

There are millions of distressed homes in probably just California alone. Please look for unkept front lawns, FSBOs (For Sale by Owner), and seek out distressed property lists that may include mortgage, homeowners, and property tax lien lates.

Network with groups like ours and share business cards with your sphere of influence which include details about how you offer quick cash for homes. If you have an exceptional deal but no cash, please bring the deals to our next meetings or email them to me.

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/trends.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-08 01:51:002023-08-08 01:51:05Top 10 Housing, Financial, and Government Trends

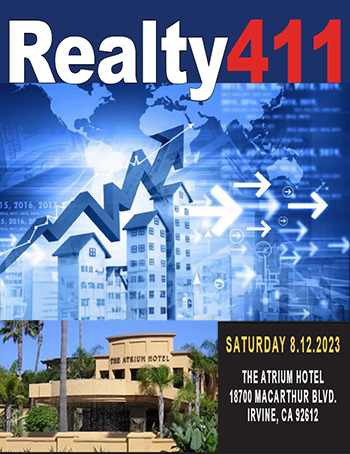

Attention real estate investors, broker/agents, private lenders, and REI professionals, Realty411 has exciting news regarding their upcoming In-Person Event in Irvine, California.

Our special one-day conference will host incredible educators from

around the country, who are ready to share their valuable insight.

Be

sure to pencil this event on schedule now. Sophisticated investors

won’t want to miss out on the updated news on both local and national

markets, real estate trends, plus the latest industry information.

article continues after advertisement

Don’t

forget about this brand-new event designed to share the latest news on

real estate investing. Our educators will be providing valuable insight,

including:

Kaaren Hall, uDirect IRA Services, LLC

Hector Padilla, HP Capital Investments

Christopher Meza, Real Titan Acquisitions

Paul Finck, The Maverick Millionaire

Rusty Tweed, TFS Properties

Barry Duron, AltLender Mortgage

Jeremy Rubin, The Friendly Flipper

Kris Miller, Legacy Wealth Strategies

Deborah Razo, Women’s Real Estate Network

Julie Harrison, Buy Direct Mississippi

Emily Nesselroad, 3 Fives Properties

Paul Wilkins, Approved Inheritance Cash

Jim Edenfield, Invest Success

Tim Emery, The Great Mile High Real Estate Investors Summit

AND MANY MORE!

article continues after advertisement

Be sure to join us IN PERSON. We will have wonderful resources, plus guests will have access to private capital, and business and commercial funding as well. We have investors joining us from across the nation for one day of networking.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/Irvine-Wealth-Summit.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-07 02:49:332023-08-16 01:26:35LEARN FROM SOPHISTICATED NATIONAL INVESTORS JOINING US IN SOUTHERN CALIFORNIA

New modern new home community in Michigan features stunning architectural and interior design

ANN ARBOR, Mich., Aug. 02, 2023 (GLOBE NEWSWIRE) — Toll Brothers, Inc. (NYSE:TOL), the nation’s leading builder of luxury homes, today announced the grand opening of its model home at Concord Pines of Ann Arbor, a new single-family community of luxury homes in a wooded enclave just minutes from downtown Ann Arbor, Michigan. A limited number of home sites remain available at the community, as well as quick move-in homes that will be ready for delivery in early 2024.

ADVERTISEMENT

The highly anticipated Buckley Modern Farmhouse model home features innovative architecture complemented by stunning interior design and merchandising, showcasing the perfect blend of luxury and modern contemporary design. Toll Brothers architecture is unmatched in the area, with homes in Concord Pines featuring open-concept single-story ranch or two-story floor plans ranging from 2,300 to 3,500 square feet and 3 to 6 bedrooms. Homeowners will enjoy well-appointed gourmet kitchens, luxury primary bedroom suites, convenient bedroom-level laundry rooms, private home offices, first-floor guest suite additions, and much more.

“Our Concord Pines of Ann Arbor community is now offering the final opportunities for our luxury single-family home designs in a prime Ann Arbor location,” said Isaac Boyd, Division President of Toll Brothers in Michigan. “The newly opened model home serves as an inspiration for our home buyers who are looking to create just the right space for their family to call home.”

The community is located in the top-rated Ann Arbor School district and next to the acclaimed Greenhills School. The central location provides residents with high-end shopping, dining, and entertainment opportunities in Downtown Ann Arbor, as well as numerous recreational options including hiking, biking, and golf. This community is also a short drive to the University of Michigan campus and medical center.

Concord Pines of Ann Arbor has experienced tremendous interest from new home buyers. Only six to-be-built home sites remain in which home buyers can choose their home design, and three quick move-in homes already under construction are available for sale with delivery dates in early 2024.

Home prices start in the low $800,000s.

For more information and to schedule an appointment to visit Concord Pines and tour the new Toll Brothers model home, call 866-267-0537 or visit ConcordPines.com.

ADVERTISEMENT

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/CONCORD-PINES.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-04 02:56:492023-08-04 02:56:53Toll Brothers Model Home Opens in Concord Pines of Ann Arbor Luxury Home Community