Universal Commercial Capital 8907 Warner Avenue, #145, 92647, Huntington Beach

BRE#:01217502 NMSL#:1730798

Realty411.com has assisted companies of all sizes expand their visibility and grow their business since 2007. Contact us for a complimentary marketing session: CLICK HERE.

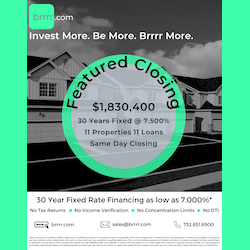

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/06/Izzy.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-06-06 05:37:052024-06-06 05:44:01Asset-Based Loans — Fast Funding

As we progress through 2024, the multifamily real estate sector continues to experience significant transformations, shaping a landscape brimming with both challenges and opportunities.

This detailed analysis delves into the seven pivotal trends that are not only redefining the multifamily market in the current year but are also expected to influence the sector well beyond 2024. Providing a comprehensive guide, this overview caters to investors and industry professionals aiming to navigate these evolving dynamics effectively.

article continues after advertisement

1. Historic Surge in Multifamily Construction

The year 2024 stands out for its record-breaking pace in multifamily construction, with the completion rates of new units reaching unprecedented levels. This boom is the result of a robust pipeline of projects initiated over the past few years. However, a recent deceleration in new construction starts—prompted by economic shifts, including interest rate adjustments—hints at a potential contraction in the pipeline by 2025. Currently, the market faces heightened competition as a flood of new properties enters the scene.

2. Rental Market Stabilization and Growth

Following a period marked by extreme volatility, the multifamily rental market is poised for stabilization. Predictions indicate a gradual increase in rental rates, fueled by a stable employment landscape, sustained housing demand, and ongoing economic uncertainties. The expected rent growth, while modest, suggests a market moving towards equilibrium, balancing out the rapid fluctuations experienced previously.

3. The Shift Towards Long-term Rentals

A significant trend reshaping the multifamily market is the growing preference for long-term rentals over homeownership. This shift is largely driven by the prohibitive mortgage rates and general unaffordability in the home-buying sector, which has broadened the demographic profile of renters to include those who might traditionally opt to buy. This demographic evolution offers real estate operators a chance to cater to a burgeoning market segment with specialized services and amenities aimed at long-term renters.

4. Impact of Hybrid Work Models

The adoption of hybrid work arrangements is significantly influencing multifamily housing preferences. As more people engage in remote or hybrid work, there’s an elevated demand for living spaces that accommodate home offices. Additionally, there’s a noticeable shift in preference towards multifamily locations further from conventional business districts. This shift provides an opportunity for real estate developers to innovate in property design and amenities, addressing the needs of a workforce that values flexibility and convenience.

5. Advancements in Property Search Technologies

The role of advanced technologies, particularly AI, in enhancing multifamily property searches is expected to expand in 2024. Building on the technological advancements of recent years, AI will increasingly influence how potential renters and buyers explore the property market, offering AI-powered search tools, virtual tours, and personalized recommendations. These technological advancements promise to make the property search process more efficient and tailored to individual preferences.

6. Emphasis on Environmental Sustainability

Environmental sustainability is becoming a critical factor in the multifamily real estate market. A growing segment of consumers is expressing a preference for eco-friendly housing options, including energy-efficient buildings, sustainable construction practices, and features that minimize the carbon footprint of residences. Real estate developers prioritizing sustainability are likely to appeal to environmentally conscious renters, aligning with broader societal shifts towards green living.

article continues after advertisement

7. Demographic Shifts Influencing Housing

Changes in demographics, such as the aging of certain populations and the emergence of millennial and Gen Z as significant groups of homebuyers and renters, are dictating evolving housing needs and preferences. These demographic trends necessitate a variety of housing solutions, from multi-generational living arrangements to affordable options for younger adults and accessible features for older residents.

Conclusion

The multifamily real estate market in 2024 is characterized by rapid evolution and diverse opportunities. For investors and industry stakeholders, staying informed about these trends is essential for navigating the complexities of the market and leveraging the potential it offers. As the sector continues to adapt and grow, the coming year promises to be a pivotal one for multifamily real estate, driven by innovation, consumer preferences, and economic factors.

Invest with Blueocean Capital

Our mission is to empower investors in building generational wealth and passive income, leaving a lasting legacy for their families. Through our comprehensive process of acquiring, operating, and eventually disposing of large-scale real estate assets, we offer a secure alternative to traditional stock and bond markets. Our unwavering commitment lies in safeguarding and preserving our investors’ wealth while delivering exceptional growth opportunities.

If you are interested in exploring the world of multifamily real estate investing and discovering how you can secure your financial future, we invite you to visit our website and schedule a call with us. Take the first step towards a brighter and more prosperous tomorrow with BlueOcean.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/06/multifamily-housing-trends.png4731000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-06-05 04:22:452024-06-05 04:22:46Navigating the New Norm: Multifamily Housing Trends of 2024

Located across Colfax from the Anschutz Medical Campus, the new development will include 370 residential apartments and ground-floor retail anchored by Queen City Collective Coffee

Aurora, CO (June 2024) – The development team of Uplands Real Estate Partners, The Max Collaborative, and Wynne Yasmer Real Estate (the same group behind the development of One River North) is pleased to announce the opening of The Broadleaf, a mixed-use residential development located within Fitzsimons Village, across from the Anschutz Medical Campus. The development includes 370 apartments and more than 9,000 square feet of ground-floor retail space lining the boulevard within the master-planned Village. Queen City Collective Coffee has signed on to operate a café space integrated within the residential lobby. Davis Partnership Architects is the architect for the project and JE Dunn is the general contractor. Kairoi Residential has been chosen to be the property manager.

article continues after advertisement

The Broadleaf marks the second project opening this year for the development team in the greater Denver market. The partnership recently opened the iconic One River North project, a residential high rise in Denver’s River North Arts District (RiNo), which has garnered national attention for its unique architecture with a “canyon” traveling through its facade. Uplands Real Estate Partners and The Max Collaborative were both founded by members of the Ratner family, the founding family of Forest City Realty Trust, which led the transformative redevelopment of Denver’s old Stapleton International Airport. Wynne Yasmer Real Estate is a Denver-based developer whose principals, Brian Wynne and K.C. Yasmer, are both former Forest City executives.

“We’re thrilled to bring a boutique residential building with top-of-market amenities to the professionals who work and study at the Anschutz Medical Campus,” said Josh Hoffman, a principal with Uplands. “The medical campus is home to approximately 25,000 employees and more than 4,000 students, with a total of 55,000 people expected to be working or studying at the campus at full buildout. The Broadleaf will provide residents with a level of quality, design, and amenities not yet offered in proximity to the campus.”

The Broadleaf is located four blocks from the Colfax Light Rail Station, providing future residents with direct access to downtown Denver, Denver International Airport, and the southeast business corridor. The development features a robust amenity package including the only rooftop pool in the area with dramatic views of the mountain range, a state-of-the-art indoor / outdoor fitness center, coworking spaces, a pet spa, bike storage with workshop, a boutique coffee shop, and secure garage parking. A half-acre outdoor courtyard will provide an urban oasis with grills, picnic tables, lounge seating, lush landscaping, and outdoor lawns for yoga and exercise.

article continues after advertisement

At seven stories, The Broadleaf is the tallest residential building in the submarket. It is the only residential building in the submarket constructed from light-gauge steel, providing superior acoustics and less sound between residences. The meticulously designed residences feature best-in-class finishes and offer one-, two- and three-bedroom apartments ranging in size from 500 square feet to 1,600 square feet.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/06/pool.png5711000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-06-04 04:49:222024-06-04 04:49:25The Broadleaf mixed-use residential development opening at Fitzsimons Village

The Myth:“You need money to invest in real estate.” The Truth: Find a good real estate deal, and the money will find you. Ask any experienced investor and they will tell you that a lack of funds is never an issue; lack of good deals is! If you can negotiate a good price on a house, you will find plenty of partners or lenders willing to put up the money.

Myth 2: No Time

The Myth:“I’ve got a job, a spouse, kids, and little spare time to invest.” The Truth: Turn off your television and you’ll have all the time you need! People spend an average three hours per day in front of the tube. They spend even more time on weekends. Want to do something fun this Saturday? Load the kids in the mini-van and drive around looking for ugly houses. Make a game out of it giving a dollar to each of your kids that spots an ugly house. Tell them that each ugly house you buy means enough money to take them all to Disneyland.

article continues after advertisement

Myth 3: Everyone Says This Stuff Doesn’t Work

The Myth: “Those late night infomercials and reality shows don’t work” The Truth: You can convince yourself that anything won’t work. Henry Ford once said, “Whether you think you can or think you can’t, you are always right.” If you listen to the critics, the naysayers, and other pessimists, you’ll convince yourself it doesn’t work. Most people that criticize money-making ideas need to do so for their own ego. After all, if it were true, what’s their excuse for not being successful? Make a point of not taking financial advice from anyone who makes less than you do.

Myth 4: Too Much Competition

The Myth: “There’s too many people trying to buy houses to find a deal.” The Truth: There are more than enough deals to make everyone successful. At any given time there are hundreds of distressed properties for sale in your market for each investor looking for them. Besides, a majority of people who say they are investors are just sitting on the sidelines waiting for something to fall in their lap. Don’t be one of them – go out and make deals happen! You will be successful if you spend your time finding deals and not worrying about other people.

Myth 5: It Doesn’t Work in My Market

The Myth:“It doesn’t work in my city.” The Truth: It works in EVERY market. True, it may work differently in some markets than others, but there are investors making money in every city, every day of the week. You have to learn your market – the rents, the trends, the local customs, the lenders, the title companies, etc. Then, learn the techniques and adapt them to your market. If you are in a hot market, you can buy and sell properties faster and ride inflation. If you are in a down market, you can find lots of bargains. Regardless, in every market, there are people with financial problems that are forced to sell their homes.

Myth 6: The Recession is Coming

The Myth: “Although the market is good right now, I hear that we are heading for another recession.” The Truth: There are always naysayers predicting market crashes. You need to ignore these pundits. Besides, there are always deals regardless which way the market is heading. If the market changes, change your strategy. For example, if the market falls, sell cheaper or with attractive terms. When Dell wants to move more computers, they drop the price. When GM wants to move cars, they offer no-interest financing. Be creative and do things that make your houses sell or rent faster. If prices are falling, buy way below market and sell just below market. If rental vacancies go up, offer free cable or WiFi. After all, when everyone else is “dooming and glooming,” it only clears out the competition.

Myth 7: Realtors Won’t Cooperate With Me

The Myth:“Real estate agents don’t cooperate with investors.” The Truth: The right agent can be your best friend and #1 source of business. I have one agent that brought me six deals in the past year. She knows exactly what I want and only calls me when there’s a deal. You need to educate a few agents and let them know exactly what you want. Few agents have repeat customers. In contrast, you have to make them understand that you will be giving them business over and over again.

Myth 8: I Have Bad Credit

The Myth: “I need good credit to buy houses.” The Truth: Good credit helps, but you don’t need it to make money in real estate. Lease/options, owner-financing, flipping properties, assignments, and other creative techniques will allow you to buy real estate without credit. Besides, you can always use a partner who has good credit. You can also borrow “hard money” without having good credit. In the interim, you can work on fixing your bad credit so you can use it as an asset in the future.

Myth 9: I Might Lose Money

The Myth:“Real estate is risky. I could lose everything.” The Truth: Real estate is one of the safest investments you can make! The stock market is beyond your control. Savings, CDs, money market funds won’t earn you enough money to make it worthwhile. You have to be willing to take a calculated risk to make money. The more you educate yourself, the less risky real estate becomes. However, don’t think you need to know everything before taking action.

article continues after advertisement

Myth 10: I Don’t Know What To Do First

The Myth:“I need to learn more before I start.” The Truth: If you’re reading this, you probably know more than enough to get started in real estate. After all, you’ll never learn everything. Knowledge is an ongoing learning process, not a result. Read books, attend seminars, and take action. Then, learn some more and take a lot more action. If you are really impatient, enlist the help of others.

Henry Ford said, “Why should I clutter my mind with general information when I have men around me who can supply any knowledge I need?” Henry Ford was a smart man because he realized that he didn’t need to know it all if he could consult with others that did. And this was before Google!

Now go out there and start submitting offers. Remember, you won’t catch any fish if you don’t put your hook in the water.

Lloyd Segal

After practicing law for over 30 years (specializing in real estate litigation), Lloyd Segal assumed the leadership of the Los Angeles County Real Estate Investors Association in 2017 from the late Phyllis Rockower. Lloyd is an author, real estate investor, mentor, public speaker, and landlord. He is the also the author of four real estate reference books, including “Stop Foreclosure in California” (Nolo Press), “Stop Foreclosure Now” (American Management Association), “Foreclosure Investing” (Regency Books), and “Flipping Houses” (Regency Books). The Los Angeles County Real Estate Investors Association is the oldest (1996) and largest investor group in California. In his role as President, Lloyd is busy expanding LAC-REIA’s events and programs for members and real estate investors. For more information, visit www.LARealEstateInvestors.com

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/06/top-ten.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-06-03 05:39:502024-06-03 05:39:51Top Ten Myths Preventing People from Investing In Real Estate

Are we currently experiencing the best economic boom ever with all-time record high stock and real estate prices? Or are more investors moving their weakening dollars into hard assets like real estate, partly as a hedge against skyrocketing inflation trends? Can Quantitative Easing ever end, or have the Federal Reserve and US Treasury created a seemingly infinite hyperinflationary spiral?

Home values have never been higher in many U.S. regions than what we’ve all seen here in 2024. The Dow Jones index also recently reached an all-time peak high of 40,000 and the NASDAQ surpassed 17,000 for the first time ever.

American mortgage holders may now have access to a staggering $11 trillion in tappable equity that’s over and above their existing mortgage balances, according to the May 2024 Mortgage Monitor report from the Intercontinental Exchange (ICE).

The amount of residential property equity is so massive that if all 48 million homeowners spent $10 million of their tappable equity each day, it would take more than 3,000 years to exhaust it, as per ICE. This amount of residential equity available is more money than the Gross Domestic Product (GDP) of Japan, India, and the United Kingdom combined.

The West Coast Gold Rush

The same ICE report identified just five housing markets on the West Coast that represented a quarter of that $11 trillion equity number: Los Angeles, San Francisco, San Jose, San Diego, and Seattle. Four of these five core equity cities are located in the Golden State of California.

As per a study released by Zillow, approximately 20% of our nation’s total housing value is in California. With an estimated 40 million residents in California and upwards of 333 Americans across the nation, the state residents represent close to 12% of all Americans. Yet, our state home values represent a much higher 20% number as compared with the rest of America.

Homeowners usually need income first to qualify for a third-party mortgage to purchase their home. While the cost of living for West Coast residents is typically near the highest in the nation, the salaries paid out by many employers, or the income generated by self-employed workers, is also among the highest in the nation with San Francisco, San Jose, and Seattle ranking first, second, and third nationally for the top average salary, according to CareerBuilder.

article continues after advertisement

The Top 5 Most Unaffordable Housing Regions

Three of the Top 5 most unaffordable housing regions in America are located in Southern California – #1 Los Angeles, #3 Irvine, and #5 Long Beach. Miami was #2 and New York City was #4, as per the RealtyHop Housing Affordability Index for May 2024.

Average families who earned the median income in Los Angeles must now spend a shockingly high percentage of 99.33% of their income on home ownership costs, as discovered in this RealtyHop survey. If true, the average Los Angeles resident would have just 0.67% (or less than 1%) of household income left over to purchase groceries and pay for utilities, automobiles, clothing, home maintenance, and other basic necessities if they were actually able to qualify for a home mortgage with those very high debt-to-income ratios.

Rounding out the Top 20 for the most unaffordable housing cities in America, which included many more California regions, were as follows:

6. Newark, NJ 7. Anaheim, CA 8. San Diego, CA 9. San Jose, CA 10. Boston, MA 11. San Francisco, CA 12. Santa Ana, CA 13. Oakland, CA 14. Chula Vista, CA 15. Fremont, CA 16. Jersey City, NJ 17. Austin, TX 18. Dallas, TX 19. Riverside, CA 20. Seattle, WA

These Top 5 most unaffordable housing regions in the survey compared the median home listing price primarily with the median income for the same region. Let’s take a look below at how high the percentage of household income was needed to cover the project monthly household expenses (mortgage, property taxes, insurance, etc.):

The Top 5 Most Affordable Housing Regions

Now, let’s review the Top 5 most affordable cities in America, which have much lower percentage of income to monthly household payment numbers:

Out of the 100 major cities analyzed by RealtyHop, a whopping 88 of the cities had homebuyers paying more than 30% of their monthly income towards household expenses.

The RealtyHop report findings were based on factors such as the percentage of income required to afford a home, a 30-year fixed mortgage rate of 7.125% (subject to change), and projected household income based on US Census and BEA data.

While there are many cities and towns across the nation with much higher median home values than the Top 5 most unaffordable housing regions listed by Realtyhop, those areas usually had much higher household income averages that helped make the home purchases more affordable.

article continues after advertisement

Income Requirements for Homes by State

Families who live in the five most expensive U.S. states for home purchases require an annual income exceeding $270,000 to live comfortably, according to a report published by Visual Capitalist.

“Comfortable” is defined as the income required to cover a 50/30/20 budget, with 50% set aside for necessities like housing and utilities, 30% for discretionary spending, and 20% allocated for savings or investments, as per the same Visual Capitalist report.

The Top 10 most expensive states for two working adults who are raising two children is listed as follows:

Because home values are so much higher today, the average mortgage balance debt is dramatically rising for many borrowers. One-to-four residential mortgage debt has also reached all-time record highs just north of $20 trillion dollars, as per the St. Louis Fed’s Economic Data.

Investments and Wealth Creation

“If you don’t find a way to make money while you sleep, you will work until you die.” – Warren Buffett

If you’re fortunate to own assets, your net worth is probably rapidly increasing. If not, the declining purchasing power of the dollar is making it very challenging for tens of millions of Americans to pay their bills on time.

There’s another old saying that is somewhat similar to Mr. Buffett’s quote that’s as follows: “Either you work hard for your money or your money works hard for you.”

Our towns, cities, states, and our nation are spending money like never before in U.S. history. The federal government continues to increase our debt at a pace of close to $1 trillion dollars every 90 days.

Between January 2020 and October 2021, the M1 money supply (cash or cash-like instruments) grew from $4 trillion to $20 trillion as I’ve written before. The more money that is created and the larger our federal debt grows and compounds, the weaker the purchasing power of the dollar.

For those people who don’t own any real estate or stocks, they are not experiencing firsthand the record wealth being created for many Americans.

Inflation is more likely than not to grow at a faster pace in the near future than what we’ve seen over the past 50 years or so. If so, real estate has proven to be an exceptional hedge against inflation as properties tend to appreciate on a historical average at least as high as the published annual inflation rates.

If you’re lucky enough to own one or more properties today, then you might consider pulling some equity out of the home to acquire more income-producing assets. For first-time homebuyers, today may be the best time to start looking for properties.

A home near you that you consider to be “too expensive” might seem very reasonable five years from now as inflation keeps rising and our dollar gets weaker and weaker.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/hyperinflation.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-31 03:06:102024-05-31 03:06:13Wealth Creation in a Hyperinflationary America

By Dan Harkey Educator & Private Money Finance Consultant 949 533 8315 [email protected] Visit my website at danharkey.com

Introduction:

“Private money, hard money, and bridge loans” are used interchangeably:

These loans refer to alternative lending sources separate and distinct from banks and institutional lending. One or more private investors/lenders fund each loan. Pools of investment capital accumulated with many private parties are also frequently used to finance private money loans. A sponsor/manager will be formed for pooled entities to fund many loans and manage the servicing.

Private money lending stands out when traditional banks decline, or the loan transaction is non-bankable. It’s a solution for property-related issues that need to be resolved, such as completing a partially constructed building or increasing occupancy in an income property with excess vacancy.

Transactions where private money loans benefit borrowers.

*Fast loan approval with possible 2-to-4-day funding for bank declines and fallouts: The bank may already have done significant underwriting, including opening escrow and title, obtaining an independent appraisal, and completing the application and financials. Some private lenders can use the banks’ information to fund faster, particularly when they have a mortgage pool or immediate capital available to invest.

*Debt consolidations for consumers, businesses, or a combination of both: In most cases, a funded loan is used for debt consolidation, lowering the borrower’s monthly payment obligations. The funded loan should give the borrower some breathing room to improve their credit and obtain a long-term bank loan. Also, if the loan is a second lien, the average interest rate between the first and second is calculated to show a ”net-effective rate.”

article continues after advertisement

*Marginal to poor creditworthiness, where a borrower is not bankable, and approval of a loan request is primarily property equity-driven.

*Special purpose-unique properties– Churches, synagogues, restaurants, bars, automotive repair shops, body repair shops, gas stations, and other single-purpose or limited properties.

*Limited document loans where the requirement is a loan application, credit report, and three to six months of bank statements. The objective is to prove the ability to pay the outstanding loan payments and other debt obligations.

*Fresh start loan. Borrowers may need to catch up and give themselves breathing room for accrued and differing payments.

*Payoff loans coming due or past due: Refinance and pay off existing first, second, and third lien position loans that may be due. Sometimes, refinancing the second and providing cash out is the appropriate answer to the loan request. Loans are available for both owner and non-owner-occupied residential and commercial properties.

*Cash-out for any reason refinances based upon the protective equity of existing real estate. Proceeds may be for business and consumer purposes. The Federal Government and some states, such as California, require a special license to engage in consumer-purpose lending.

*Junior lien or second-position loans on both owner and non-owner-occupied dwellings for business purposes.

*Construction completion, rebuilding, or upgrading properties in poor or marginal condition: The loan is usually necessary because the collateral property or the borrower needs to meet bank underwriting guidelines in its distressed or partially completed state. Loan approval by the lender will consider the as-is-value and the as-completed-value.

*A borrower may own and operate a cash-based small business with limited financial strength, as the books show. A lender will require 3 to 6 months of personal and business bank statements. The borrower must still prove that they can make the required payments.

*Leveraged existing real estate equity developed over time to borrow additional funds, purchase other investment properties or invest in a business enterprise.

*Purchase a property with some cash down payment, sweat equity, and seller’s agreement to carry back a subordinated junior lien. The property seller would have the borrower sign a promissory note and a deed of trust with a set interest rate, payment schedule, and due date. The subordinated second is recorded concurrently with the first trust deed but with a recording number after the first.

*Inherited property where family members and successor trustees who are beneficiaries need funds for distribution to the beneficiaries, pay the estate’s legal costs or fix up the property for a future rental. Another option is fixing it and selling it on the open market.

*Loan on unimproved raw land. Loaning on raw land can be a complex process. Is the land parcel part of an existing subdivision, referred to as an infill lot, a commercially or industrially zoned parcel within a subdivision, or a larger parcel held for future development? The borrower may need to use the property as collateral to raise funds for future entitlements, including engineering, architecture, various reports, and fees to develop a fully entitled parcel ready to be built. The borrower would pay the loan off as part of the construction loan.

article continues after advertisement

*Retail strip and community centers, industrial or other properties that require upgrades or repositioning: Many centers are distressed due to the COVID shutdown vacancies, where tenants could not pay rent.

*Fix-and-flip loans allow high-frequency purchasers to purchase a distressed property, rehabilitate it with the expectation of resale, and turn a quick profit. Borrowers need both experience and some of their capital at risk.

*Litigation settlements: A loan to buy out a business partner, pay off a pesky family member, an ex-spouse, a judgment lien, or a partition suit.

*Pay off civil judgments and liens, including arrearage in property taxes, association dues, and federal and state tax liens.

*Sale of existing promissory notes and deeds of trust to 3rd party investors: The sale is usually at a discount, whether the promissory note is performing or non-preforming. A deal will free up cash.

*Hypothecation or pledge of a promissory note and deed of trust: A borrower who owns a promissory note and deed will assign them to a third-party investor as collateral for a new loan.

*Cross-collateralization of more than one property: Multiple properties are required to meet the lender’s equity requirements. The borrower would sign one promissory note but have recorded liens that encumber two or more properties.

*Small mobile homes or trailer parks: properties that don’t meet the underwriting standards of institutional lenders.

*Vacation, Short-term, and rental income properties; Financials and history are necessary to prove the ability to make payments.

*New ground-up construction or construction completion for a partially completed project: Most requests result from borrowers needing to fund additional dollars to complete the project when they deplete their capital or existing construction loan proceeds.

*Collateral combines real and personal property, such as a motel, restaurant, carwash, or gas station with mini markets. A recorded trust deed encumbers the real property, and a UUC-1 financing statement will be filed with the Secretary of State to encumber the personal property. The valuation and decision to make the loan must be on the real property only.

*A long-term lease on commercial property has or is expected to expire soon. The lease expiration could cause a vacancy and a disruption in rental income. If the master tenant vacates the property, this will disrupt other smaller in-line tenants because the master tenant is responsible for the primary draw of foot traffic to the center. Banks will usually not make this loan. This loan is generally a bridge loan until the owner obtains a long-term lease with a credit-worthy tenant and manages the center back into stabilization.

*Credit approval is subject to highly sophisticated lease analyses, with multiple tenants having different lease terms, including length, lease rate, and lease provisions. Some tenants are on long-term leases, and some are on a month-to-month tenancy. Lease documents may include go-dark requirements for the anchor tenant or provide for lease cancellation in the event of excess vacancy or loss of an anchor tenant.

*Some properties require mutual property access easements for ingress/egress or complex usage rights, such as reciprocal parking agreements. Many properties, such as churches and retail shopping centers, sign contracts with multiple property owners to use the entry/exit of the property or the parking in specific ways or at certain times.

*Foreign nationals with and without social security. The borrower must have a U.S. bank account(s). The borrower must have a process agent service arranged during loan processing.

*“Notice of a substandard condition” or “notice of property noncompliance” is recorded on public records by a building department notifying the public that the property is out of conformance or in disrepair for building and zoning codes. The bridge loan funded by private lenders will provide funds to make substantial improvements and modifications to bring the property up to acceptable building, safety, and zoning standards. Institutional lenders will not make these loans.

*Non-conforming property does not comply with current zoning and building standards. As a result, strict limitations exist on repairing or replacing structures in destructive acts such as fire, flood, windstorm, vandalism, or earthquake. The property may not be able to be rebuilt to an acceptable level after the destructive event occurs.

*Earthquake seismic retrofit. Many older properties require upgrades, such as engineered reinforced steel frames bolted into the existing structure and walls shored up with steel support fasteners to withstand earthquakes.

*Tenant improvements. Commercial building owners must provide funds to install interior or exterior improvements to satisfy the owners’ and prospective tenants’ leasehold improvements.

*Cannabis-related properties, manufacturing, and retail facilities: Some states have legalized lending in cannabis-related operations, and others have not.

In summary, private money loans are collateral-driven, even though the lender must review the borrower’s financials to prove that the borrower can pay the debts.

If you find value in this article, please forward it to friends and associates. You may use this article in your marketing efforts.

Thank you

Dan Harkey

Dan Harkey

Dan Harkey is a contributing author to Weekly Real Estate News and is a Business & Financial Consultant. He can be contacted at 949-533-8315 or [email protected].

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/hard-money.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-30 03:17:582024-12-05 06:35:18Private Money, Hard Money

“Hospitality-infused” office building at 2nd & Adams in Cherry Creek predicted to be 70 percent leased at the start of construction

Cherry Creek North, CO (May 2024) – Magnetic Capital is proud to announce the groundbreaking ceremony (please see invitation in email for details) for Cherry Creek’s newest office building, located at 2nd & Adams. The 100,000 square foot, “hospitality-infused” building is expected to be 70 percent leased at the start of construction, including a 30,000 square foot lease to Bow River Capital.

article continues after advertisement

“We’re very excited to announce the start of construction for 2nd & Adams, and provide our tenants with an office building that is designed and configured with the ultimate in hospitality in mind,” said Chris Carroll of Magnetic Capital. “Cherry Creek represents a ‘flight to quality’ among businesses that want a safe, friendly and first-class location where their employees can live, work and play. While downtown Denver continues to struggle with office vacancies, Cherry Creek has experienced 65 percent rent growth since Covid and a steady influx of new office and retail tenants, as well as residents filling existing and new multifamily communities.”

Bow River Capital, a Denver-based private alternative asset manager, will locate the company’s new headquarters at 2nd & Adams and become the building’s anchor tenant.

“We’re thrilled to be moving Bow River’s headquarters to 2nd & Adams and to be the first of many companies that will enjoy the building’s forward-thinking design,” said Bow River Capital Chief Operating Officer Jane Ingalls. “We were drawn to the focus on hospitality and elevated common areas that 2nd & Adams will provide to our team and guests.”

Construction of the mixed-use office development is scheduled for completion in the third quarter of 2025. The project will include approximately 80,000 square feet of office space and 20,000 square feet of retail. The development team is focused on what it calls a “hospitality-infused office operating model” with a heavy emphasis on food and beverage and the broader activation of common areas. The project will have multiple food and beverage and retail concepts across the ground floor and the rooftop will feature a 5,600 square foot bar and restaurant, anchored by best-in-class national operators.

OZ Architecture is the architect for the project and Mortenson Construction is the general contractor. OZ Architecture recently released an article on the project here. Blake Holcomb at CBRE is handling office leasing and can be reached here.

Cherry Creek North Dynamics: Cherry Creek North’s unique concentration of high-end retail, executive housing, luxury multifamily, and premium hotels, all within a 16-block radius, positions it among the top office markets in the US today. With a vacancy rate of sub-2% and physical occupancy at ~95%, Cherry Creek contains fundamentals comparable to Sand Hill Road, Beverly Hills, and Century City. More information regarding Cherry Creek North is available at www.cherrycreeknorth.com.

About Magnetic Capital Magnetic Capital, led by Dan Huml and Chris Carroll, is a privately held real estate investment and development company focused on developing and operating real estate assets often overlooked or undervalued by traditional investment firms. Headquartered in Denver, Colorado, Magnetic Capital is focused on development and multifamily acquisitions opportunities along the Front Range.

About Bow River Capital Bow River Capital is a private alternative asset manager based in Denver, Colorado, focused on investing in the lower and middle market in four asset classes: private credit, private equity, real estate, and software growth equity. Through its subsidiary Bow River Advisers, LLC, Bow River Capital also offers a registered, closed-end mutual fund – Bow River Capital Evergreen Fund (EVERX) – designed to provide institutional-quality private market access to a broader set of investors. Collectively, the Bow River Capital team has deployed capital into diverse industries, asset classes and across the capital structure.

Bow River Capital Evergreen Fund is distributed by Foreside Financial Services, LLC, which is not affiliated with Bow River Capital or its affiliates.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/groundbreaking2.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-29 03:15:262024-05-29 03:15:27New Office Building in Cherry Creek Breaks Ground

Real estate investing is an extremely powerful tool for building short-term and generational wealth. This includes offering a route to financial freedom while delivering passive income. However, navigating this path successfully requires awareness of common pitfalls that can thwart even the most well-intentioned investors. With a diverse portfolio that spans from $40,000 single-family homes to million-dollar properties, I’ve gleaned valuable insights on effective strategies and mistakes to avoid. Here’s a detailed look at the smart ways to invest in real estate and the top five mistakes people often make, enriched with real-life stories from my experience and some pro tips.

1. Failing to Do Thorough Market Research

What to Do: Conduct comprehensive market research before investing in areas, especially in locations that you do not know well. Have you seen the Homes.com commercials? They joke about going undercover and doing the research for you. However, this is what you need to do especially for out-of-the-area markets. You need to understand local economic drivers, population growth trends, employment rates, and housing demand.

Is there a new casino going into the area or is a factory closing? Both can have a significant impact on the local economy and the housing market.

article continues after advertisement

Use resources like:

Local Government Websites: Access economic development reports and city planning documents. It is mainly free and open to the public. You just need to know where to look.

Real Estate Portals: Sites like Zillow, Homes.com, Redfin,PropertyShark and Realtor.com offer market trends and property value data.

Market Analysis Reports: Industry reports from companies like JLL, CBRE, or local real estate associations provide in-depth market insights.

**Mistake to Avoid:** Investors often buy properties that are cheaper but in areas with declining populations or economic instability, leading to poor returns and high vacancy rates.

Story: Early in my career, we bought a portfolio of “cheaper properties” compared to where I live in a small midwest town with the expectation of significant growth happening in the area. However, the city delayed the major growth project in the area. While other areas of the country grew 10 to 50% before or during COVID this area stayed flat. This taught me the importance of thorough market research.

2. Overleveraging and Poor Financial Planning

What to Do: Maintain a conservative debt-to-equity ratio and have substantial cash reserves. This includes:

Budgeting for Contingencies or Whoops factor: Set aside funds for unexpected repairs or vacancies.

Creating a Financial Plan: Include investment goals, cash flow projections, and exit strategies. Make sure to find out the cost of a refresh in your area.

Mistake: Overleveraging can lead to financial ruin if the market shifts or unexpected expenses arise, leaving you unable to service debt or cover costs.

Story: The real estate market will not go up forever. I learned this lesson the hard way during the 2008-2010 housing market crash. Instead of taking profits along the way by selling off some of our properties. We were caught in the downturn. We lost a few properties and had to sell others at a loss. This experience underscored the necessity of maintaining a healthy balance between debt and equity.

Pro Tip: I typically have my client’s people set aside or keep a reserve of 1% of the purchase price or 10% of the rehab budget whichever is higher when fixing a property. You should also have 3 exit strategies and not just one for each of your properties.

3. Ignoring Property Management:

What to Do: Either manage properties efficiently yourself or hire a reputable property management company. Key responsibilities include:

– Tenant Screening: Conduct thorough background and credit checks. – Rent Collection: Implement a reliable system for on-time payments. – Maintenance: Regular inspections and prompt repairs to maintain property value.

Mistake: Poor management leads to high tenant turnover, property degradation, and loss of rental income.

Story: I have lots of my clients and students who have had bad experiences because of not doing proper screening on their tenants. The least of your concern is the tenant not paying rent for 6 to 9 months. One couple that I coach wanted to be nice to their tenant and listen to a local attorney who said, “The tenant would leave after a few notices.” It had already been several months of late rent and not paying in full when they engaged the attorney. Well six months later, they finally listened to me and got the eviction process started. The tenant fought it but did move out when the sheriff finally showed up to evict them. Sometimes we have to make a hard choice.

Pro Tip: Don’t be cheap and make sure to do background checks on your tenants.

4. Skimping on Due Diligence

What to Do: Perform your due diligence before purchasing and use professionals even if not required in your state. This includes:

– Property Inspections: Hire professional inspectors to check for structural issues, pest infestations, and compliance with safety regulations.

– Hire Attorney to Perform Legal Checks: Ensure there are no liens, easements, or zoning problems.

– Surveying: Verify property boundaries and land use restrictions.

Mistake: Failing to uncover these issues can result in costly legal battles, unexpected repair expenses, or inability to use the property as intended.

Story: This is one of the biggest things that my clients and students want to push back on in states where attorneys are not required to purchase a property. Do not be CHEAP as there are lots of horry stories. I would much rather pay an attorney $750 to $1,500 to do a closing than find an issue later the cost $20,000 to $100,000+ to fix or even worse an EPA issue. I was just talking with someone buying their own home that had asbestos only in their floor. Anything EPA related will most likely cost 25%+ more than you expected and take longer 30 to 90 days longer to fix than you planned. So, be prepared. The government does not move fast.

5. Underestimating Costs

What to Do: Accurately estimate all costs involved. This encompasses:

– Closing Costs:** Fees for legal services, title insurance, and loan origination.

– Renovation and Repairs:** Obtain detailed estimates from contractors.

– Ongoing Expenses:** Property taxes, insurance, utilities, and maintenance.

Mistake: Many first-time home buyers and investors focus solely on the purchase price, underestimating the total investment required, leading to cash flow issues. Most people are shocked by all of the closing costs on their first deal.

Story: On my first home, I did not review the HUD (Now, closing statement) before my closing but that is the time to see all of the expected costs on the closing of your home or property. I ended up paying an extremely high fee to my mortgage guy. My attorney caught it at the closing but it was too late to change it for the purchase.

Pro Tip: Make sure to review all of your fees on the documents you sign before closing. Make sure to have your professionals outline their fees upfront.

article continues after advertisement

**Conclusion**

Real estate investing is a powerful tool for building wealth and achieving financial independence, but it requires careful planning and informed decision-making. By avoiding these common mistakes and following strategic investment practices, you can enhance your chances of success and meet your financial objectives. For more insights, Pro Tips, and detailed guidance, visit [www.hughzaresky.com](http://www.hughzaresky.com), where I share my experiences and tips from decades of real estate investing.

Happy investing!

Hugh Zaretsky

Hugh Zaretsky, was an IT executive until his wake-up call came on 9/11. Realizing how short life can be, Hugh transitioned his career to become a real estate investor, international speaker, best-selling author, philanthropist, and advocate for empowering individuals. Hugh started investing in the precursor to Short-Term Rentals back in 2005. His expertise in cash-flowing properties (STR, SFH, and multi-family) has allowed him to successfully train over 12,500 real estate investors and entrepreneurs to complete profitable real estate transactions, launch businesses, or take them to the next level.

Hugh has been a certified real estate continuing education instructor in 4 different states. His latest book “The Launch Button” was an Amazon best seller in 4 categories including all of real estate. He recently spoke at the Humanity Summit in Portugal on the global issue of “Sustainable tourism (including STRs) and how to work with local communities”. His dedication to mentoring and coaching aspiring entrepreneurs makes Hugh a highly sought-after coach, trainer and speaker. Get ready to be inspired and gain invaluable insights from Hugh’s wealth of experience. To learn more about Hugh go to www.HughZaretsky.com

www.thelaunchbutton.net or buy direct on Amazon. – My book “The Launch Button” is an amazon best seller helping people find their passion or take their business to the next level.

“You have to change your mindset before you can change the size of your wallet.” – Hugh Z

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/wealth-1.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-28 05:42:392024-05-30 01:43:06Unlocking Wealth: 5 Real Estate Mistakes to Avoid for Smart, Passive Income

You’re invited to National Private Lender Expo® Commercial Real Estate Conference Thursday May 30, 2024 Antuns, Queens Village New York 3:00pm to 8:00pm

View video clips of the past National Private Lender Expo®

Schedule a call for sponsor, on-stage speaking engagements, PowerPoint presentations

It’s truly an honor to have these distinguished, illustrios indiividuals provide powerful presentations live on-stage at the National Private Lender Expo commercial real estate conference in the heart of the five boroughs of New York. If you’re involved in the private lending industry, you’ll make priceless connections in a royal atmosphere at this annual flagship event attended by private lending professionals, accredited investors, major commercial real estate players from across the continent.

Follow our company page to keep apprised of the latest news in the private lending industry.

This flagship event is organized by Peretz Toiv – CEO HardMoney.com Follow Mr. Toiv on LinkedIn

Antuns is located directly across the street from the LIRR Queens Village Station and near Mass Transit. Three free parking lots for your convenience. Bring lots of business cards:)

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/conference-1.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-27 04:37:462024-07-01 05:58:07You’re invited to National Private Lender Expo® Commercial Real Estate Conference

The following is an example sequence of questions that loan agents can use to obtain the information from the borrower. These are suggested. Each loan agent may set up their questioning sequence, which will vary but accomplish the same result.

Conversations with borrowers may be fluid and take the loan agent into complex life stories to obtain intended information. I often pause to let them talk because I know they are upset, not about me but their life circumstances.

Borrowers love to tell you their life’s problems while you are attempting to obtain material facts. Compassionate listening is a natural, thoughtful, learned trait that helps develop trust and lasting relationships.

article

continues after advertisement

Any sales career endeavor involving products, goods, or services will have a similar best practices sequence of questioning. All salespeople should take the time to write down a sequence of questions as an effective platform for intended results. The intended outcome is to obtain the material facts, represent the customer with good intentions, explain and answer questions, determine the transaction’s viability, and close and drive the transaction forward. Or decline the transaction if it does not fit the company’s requirements.

Educating a client or customer is part of the job of any professional salesperson. The customer should come away with the idea that the salesperson honestly had their best interest in mind. A byproduct of this philosophy is a lasting relationship, spreading goodwill, and referrals.

Stage I: Questions as a best practices platform include:

• Loan amount, for what term?

• First or second lien?

• Type of property: single-family, owner- or non-owner-occupied, commercial, apartments, industrial, occupancy, or other.

• Loan purpose: This question is paramount if the loan request is single-family owner-occupied. Is the use of loan proceeds primarily for business purposes? Primarily means 51% or more of the loan proceeds. What portion will be used for consumer purposes?

• Where is the property located?

• Property value. How did the borrowers determine the value? A borrower’s estimate of value is often incorrect or intentionally exaggerated.

• Cash out requested?

• Current total liens

• Are the liens current? If not, how much is the arrearage and the reason? Get the complete story in writing. Completeness may make or break your transaction. Some reasons may be rational, while others are just an attempt to conceal.

• Loan-to-value: LTV ratio total loans divided by appraised property value (APV)

• Description of collateral property.

• Property address

• Exit strategy: What are the borrower’s plans to repay this loan?

• Rental income stream? What gross rents, vacancies, and expenses are required to determine net operating income, often called NOI? The NOI calculation excludes debt service. Will the NOI cover the loan payments and property expenses?

• Most recent payment statement(s)-Please obtain.

• When was the property purchased, and for how much?

• Have they made any significant improvements or upgrades? Please provide a list of upgrades and costs.

• Pictures of the outside and inside: In most cases, pictures are found online, with Zillow, Redfin, Realtor.com, and Trulia. Photos of the inside and outside are necessary if the property has undergone significant upgrades that enhance its value.

• Is the property owner/borrower a private individual(s) or an entity? If an entity, what is the purpose of the enterprise?

• If the property is newly or partially reconstructed, inside and out pictures are necessary, as well as a list of improvements, costs, and what improvements remain to be completed.

• Any exceptional circumstances? Weaknesses in the transaction include a history of late payments, significant arrearages in payments, accrued unpaid property taxes, outstanding judgments and liens, state and federal taxes due, probate sales, bad credit, open bankruptcy, pending divorce proceedings, tax liens or judgments, the property has a recorded notice of substandard condition, red tagged for code violations, successor trustee acting on behalf of a family trust, multiple borrowers, multiple cross-collateralized properties, etc.

article continues after advertisement

• Forward the prospective borrower a loan application and authorization to obtain credit. Request the most recent property loan payment statement and at least three months of bank statements. Use a commercial loan application rather than a 1003 residential form when possible.

• Ask for a handwritten purpose of the loan letter.

• Does the borrower have an online presence? If they are a company, they may have a website. If they are individuals, they may have a presence on LinkedIn. Does the borrower have a promotional summary about themselves? Add these items to the executive summary sent to the lender. Positive promotional material will add credibility to the prospective borrower.

The above information is sufficient for the loan agent to write an executive summary and email it to a prospective lender. Then, follow up with a phone call.

Stage II: Driving the loan process forward:

• Private money vs. institutional lenders have different borrower requirements, requiring tax returns, recent pay stubs, w-2s, and 1099s.

• Profit, loss, and financial statements are necessary if the borrower is an operating entity. Two data sets, one for personal and one for business, may be required separately.

• In addition to a borrower’s signed letter of interest, loan application, and credit authorization, the agent will need other data, such as a property owner family trust document, an operating statement for a limited liability company (LLC), insurance broker contact information, and association management company contact information.

• If the loan request is for a junior loan, information about the senior loans will be required. Documents for review may include a copy of the promissory note, loan agreements, and a recent payment statement from the senior lien holder or loan servicer. Reviewing the recorded documents related to the senior lien associated with the deed of trust is prudent.

• Does the first lien have a written provision in the deed of trust referred to as an “alienation clause” or a “due on further encumbrance clause” that would require the lender to obtain written approval to place a junior lien on the property? If the loan agent is working on a second lien loan, they should review the deed of trust and the loan agreement to see if there is a prohibition of placing a junior lien without obtaining the first lien lender’s approval.

This fact is important because, in many cases, the original borrower may have been parents, possible deceased members, siblings, co-trustees of a family trust, ex-spouses, or other miscellaneous parties. Some earlier property purchases were taken “subject to” a lien that prior owners obtained in the past. Completing a property sale “subject to” means that the purchaser/borrower purposefully failed to notify the first lien holder of the transfer. Was the sale transfer kept a secret, deliberately to get a lower interest rate? Therefore, the loan documents still show the obligor as the prior owner on the note and deed of trust.

• Does the person requesting the loan have the sole authority to borrow and encumber the property with a new lien? Are there other parties of interest who may object to recording a lien on the property? An estranged ex-husband, ex-wife, business partner, or trust beneficiary would be an example.

• Are there multiple borrower parties that a lender must include in the application, processing, underwriting, and closing process? A lender’s frustration will occur when the discovery that the borrower has intentionally excluded an undisclosed hostile party. I assure you that an unknown borrower party will not fool a good loan processor or the title company. When the title insurer underwrites their coverage, they will ensure that the correct parties have signed the documents. Verifying the proper parties is part of their insurance underwriter and approval process.

• Additional documentation may be required to drive the process forward as a loan processor sets up their file. The loan agent should maintain a respectful and enthusiastic relationship with the processor.

Sifting through the maze of questions and answers to develop a well-written executive summary to send to the lender

Loan agents ask prospective borrowers questions to determine the transaction’s viability. They are responsible for obtaining specific information from the borrower or the borrower’s agent.

Some agents are responsible for asking appropriate questions but then calling a lender with fragmented and incomplete information to discuss the potential loan transaction. The lender will respond that they need more information. The agent will answer, “What do you need?”

There are dozens of questions that may be asked at the front end, but getting to the basics of whether the potential loan transaction is viable is the beginning. Sifting through the maze of complexities includes:

Property types, income generating, and occupancies,

Agent’s competency, property ownership variables,

Borrower creditworthiness,

Borrower’s propensity to withhold material facts,

Some borrowers will withhold information, unaware they will get caught while processing the loan. A critical thinking questioning sequence will avoid most of this.

The material facts of the transaction should be summarized and submitted to a lender via email as an organized written executive summary, followed by a phone call discussion. Usually, a request for more information is anticipated. Emphasize the positives first and the negatives later. However, do not bury the negatives so the lender discovers them later.

Lenders have long memories about who is professional and honest, supply only fragmented data, and summarily leave out adverse material facts. After a couple of repeated offenses, the assumption will be that the loan agent withheld the negatives intentionally. Reputations, both negative and positive, accrue quickly. Experience, understanding, and the propensity to fully disclose and protect the lender’s interest will ensure lasting relationships.

After reviewing the material facts, the lender may express an interest or decline the proposed transaction. Or the lender may ask for more information. If you receive a positive response, that is great, and if you receive a rejection, it is a rejection of your request, not a rejection of you. Move on to the next lender. Lenders have different risk assessment standards and pricing structures. For example, some lenders require an independent third-party appraisal, and some do not. Some lenders care about FICO scores, and some do not. Some lenders need assurances about the ability to pay, while others are less concerned. Some lenders should be more skilled in processing and underwriting and, therefore, take riskier deals unknowingly.

The loan agent looks forward to a term sheet or a letter of interest. The written term sheet will state the lender’s terms and conditions to make the loan subject to an appraisal and underwriting of the material facts submitted by the borrower.

The above is helpful as a platform for questioning borrowers for adequate information to submit to a prospective lender to obtain an expression of interest, a terms sheet, or a letter of interest.

I sincerely hope that you find value in this article. If so, please forward it to your associates. Please refer your friends and associates to me at [email protected].

Thank you,

Dan Harkey

Dan Harkey

Dan Harkey is a contributing author to Weekly Real Estate News and is a Business & Financial Consultant. He can be contacted at 949-533-8315 or [email protected].

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/question-real-estate.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-23 04:53:252024-05-23 04:53:27Ask the Right Questions! To Determine the Viability of a New Loan Request