I wanted to let you know one of the people I respect the most in Real Estate, Marcella Silva…

She is hosting a special training called “Today’s Dirt Is Tomorrow’s Gold” and I just couldn’t resist telling you about it.

I wanted to reach out to you because I thought you or a friend or family member might want to learn about the best kept secret in Real Estate…Land Banking.

I KNOW you’ll get a ton out of this.

And knowing Marcella, you can bet nothing will be held back.

Here’s what you can expect when you show up:

Secret #1: The TRUTH About The Hidden Wealth In Real Estate

Secret #2: The Largest Global Shift Of Wealth

Secret #3: The Laws That Are Causing The Largest Land Rush In History

Founded in 2007, Realty411.com has assisted companies of all sizes and budgets expand their visibility and grow their business. Contact us for a complimentary marketing session: CLICK HERE. Investors, do you need a referral? Our investor network is nationwide: CONTACT US – Ph: 805.693.1497 – Text: 310.994.1962 – CA DRE # 01355569

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/10/money-grow.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-10-15 02:12:472022-10-15 02:12:50Ready to Find a Good Investment?

Boulder, CO (October 11, 2022) – Evermore Partners (Evermore), a real estate investment company focusing on high-impact, value creation activities, has announced the company’s purchase of 6707 Winchester Circle, a 33,296 SF office/flex building proximate to its acquisition of another property in Boulder earlier in 2022.

ADVERTISEMENT

“The acquisition of this property is another great step for our company and its acquisition goals,” said Founder and CEO Seth Wolkov. As long-term believers in the Boulder area, we’re confident that this type of product will have enduring demand and relevancy. The combination of modern office layout, recently built out life-science lab space, and dock-door equipped distribution space will appeal to many types of tenants over time and provide good downside protection.”

The Evermore team has acquired over $1 billion worth of assets through multiple economic cycles, in all product types, and has specific experience with value-add and distressed and opportunistic investing. Evermore’s goal of acquiring a $250 million real estate portfolio in the Rocky Mountain Region within five years will be accomplished with assets sized between $5 million and $50 million across five key product types located within urban, college and core mountain communities.

ADVERTISEMENT

Evermore focuses on markets located at the intersection of “Eds, Meds and Technology” that continue to experience above average net migration, wage and employment growth, helping to drive investment returns. The company seeks double-digit total returns generated from a combination of current cash yield and capital appreciation.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/10/photo-6707-Winchester-Evermore-Partners.jpg459723dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-10-13 06:08:472022-10-13 06:08:50Evermore Partners Acquires Second Flex/Office Property in Boulder

It’s time for another informative REI (Real Estate Investing) Wealth magazine. For our 59th edition, we feature a prominent physician turned real estate investor and mentor: Dr. Chander Mishra, along with his wife and investment partner, Iva.

This power couple are on a mission to help spread real estate investing knowledge, especially in the healthcare industry. Inside our jam-packed issue readers will discover educational articles and companies ready to assist them in their REI journey.

Be sure to download our latest REI Wealth issue, CLICK HERE!

Founded in 2007, Realty411.com has assisted companies of all sizes and budgets expand their visibility and grow their business. Contact us for a complimentary marketing session: CLICK HERE.Investors, do you need a referral? Our investor network is nationwide: CONTACT US – Ph: 805.693.1497 – Text: 310.994.1962 – CA DRE # 01355569

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/10/issue-59-banner.jpg12502033dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-10-07 11:10:442022-10-07 11:15:13New REI Wealth Issue #59 is LIVE – Download it Here!

Why can’t commercial lending be as flexible as residential lending? Residential mortgage lending for one-to-four unit properties has become more automated and streamlined for investors as we move forward here in the 21st century. More homeowners and investors are seeking out experienced independent mortgage brokers who may have relationships with numerous financial institutions, nonbank lenders, or private money sources. With a few clicks of a button, the mortgage professional can quickly find the best financial solutions available for their clients and get approvals within minutes, hours, or days.

Commercial property lending, on the other hand, still seems stuck in the 20th century for many commercial applicants. It can be perceived as a “good ol’ boy/girl network” in that the commercial loan applicant needs to have some sort of a long-established personal relationship with their local community banker dating back to high school, college, or as fellow members at the local golf club before their loan requests are approved. If so, will they be types of friendly handshake approvals or not-so-friendly “take it or leave it” approvals?

ADVERTISEMENT

If the commercial loan applicant is fortunate to find a banker who may consider their deal, this same banker may request that the borrower move their deposits from other financial institutions to their bank before considering the applicant’s loan request. Should the loan be rejected either quickly or months later after a rather brutal loan underwriting process that may include a footlong stack of paperwork, the disheartened customer may give up hope and not know where to turn for another lending option.

Today, non-owner occupied residential properties (one-to-four units) offered as short-term or long-term rentals, multifamily apartments (5+ units), mixed-use, office, industrial, retail, and special purpose (auto repair shops, etc.) can all be viewed as a “commercial loan” by certain nonbank lenders that don’t collect customer deposits like traditional banks. With lower loan-to-value (LTV) ranges for certain asset-based loan products, the risk of default is lower for the nonbank lenders.

Wealth Creation from Commercial Property Ownership

Let’s take a look at commercial property trends and how much wealth was created for those fortunate owners who learned that it’s much better to let their money work hard for them than vice versa:

The estimated total dollar value of commercial real estate was $20.7 trillion as of Q2 2021. (Nareit and CoStar)

By 2050, commercial building floor space is expected to reach 124.3 billion square feet, a 33% increase from 2020. (Center for Sustainable Systems, University of Michigan)

72% of commercial buildings in the US are 10,000 square feet or smaller. (National Association of Realtors)

The typical length of a building lease in the US is three to 10 years. (DLA Piper)

Commercial property prices rose by 20% between May 2021 and May 2022. (Green Street)

An estimated one-third of industrial space in the US is more than 50 years old. (NMRK)

For every $1 billion of growth in the e-commerce sector, it requires an extra 1.2 million square feet of new warehouse space. (Prologis)

Self-storage commercial unit REITs produced a 70% market return in 2021 (REIT)

Approximately 69% of all commercial buyers in the US need financing to purchase properties. (National Association of Realtors)

Sales of multifamily apartment buildings increased by 22.4% year-on-year in 2022 (Colliers)

Prior to the March 2020 pandemic designation, the industrial real estate sector had grown for 40 consecutive quarters or over 10 years. (NMRK)

Industrial vacancy rates nationwide fell below 3.7% at the end of 2021. (Cushman & Wakefield)

The Inland Empire (Riverside and San Bernardino counties) in California averaged an incredibly low 1.2% vacancy rate for industrial space. (Commercial Edge)

California had 27 of the 50 highest office rental prices in 2021. (Commercial Search)

The average annual return for commercial real estate investors is approximately 9.5%. (Mashvisor)

For every retail unit that closes, five new stores open up. (NRF)

Technological Advances for Commercial Loans

What if the commercial lending process could be digitized, sped up, and completed on a secure online loan application with just one point of contact? Your odds of success for getting a commercial property loan approved for a multifamily apartment building, mini-storage site, or small retail center will be much higher if your financial contact person is very experienced with commercial lending and has access to numerous lenders.

Commercial loans are somewhat like giant jigsaw puzzles. While the applicant’s loan package may not fit the guidelines required at one, two, or 10 different lenders, there are other lenders that have more flexible guidelines which allow lower positive, break-even, or even negative DSCR (Debt Service Coverage Ratio) with or without income verification.

Properties with lower positive cash flow or even negative cash flow estimates will likely not qualify at a local community bank or credit union. Yet, they may qualify with other nonbank lenders that do allow break-even or negative cash flow. Some of our lending partners are asset-based lenders that don’t review the applicant’s tax returns as well as provide financing for property improvements. These types of incredibly flexible lending guidelines can make the commercial loan application process much easier for the borrower.

ADVERTISEMENT

An Imploding Financial System and Increasing Bank Restrictions

In 2008, the Credit Crisis (aka Financial Crisis, Subprime Mortgage Crisis, or Global Financial Crisis) default risks became more readily apparent as these prominent financial institutions or government entities collapsed and/or were bailed out:

Bear Stearns: The fifth largest investment firm in the world that was heavily invested in mortgage-backed securities, collateralized debt obligations (CDOs), and other complex securities or derivatives instruments.

Lehman Brothers: The biggest bankruptcy ever involving over $600 billion in assets.

Washington Mutual (WAMU): Largest bank implosion in US history with almost $328 billion in assets.

FDIC (Federal Deposit Insurance Corporation): They only held $40 billion in cash reserves at the time of WAMU’s collapse, so the government had to silently bail them out to prevent bank runs.

Countrywide Mortgage: Once America’s #1 residential mortgage lender that almost imploded prior to being bailed out by Bank of America.

American International Group (AIG): They were the world’s largest insurance company and were bailed out by the US government starting with $85 billion while growing to more than $182 billion several years later.

Merrill Lynch: The world’s largest stock brokerage firm at the time with $2.2 trillion under management and 15,000 brokers that was taken over by Bank of America.

A derivative is a complex hybrid financial and insurance instrument which “derives” value from underlying assets or benchmarks like interest rate direction trends. Some financial analysts have stated that the total value of all global derivatives may be somewhere within the $1,500 to $3,000 trillion dollar region. If so, these derivatives dwarf all combined global assets by a significant multitude.

Because so many banks, investment firms, and insurance companies are heavily invested in one another partly by way of derivatives, this was why the Federal Reserve, the Bank of England, and other central banks around the world had to step in and bail out these multi-billion or multi-trillion dollar financial or insurance entities, directly or indirectly through others like Bank of America. If not, the global financial system would have fallen like a dominoes chain reaction.

Later, the LIBOR (London Interbank Offered Rate) Scandal, which came to light publicly in 2012, gave us a glimpse of the sheer magnitude of the derivatives market. This financial scandal was about how certain financial institutions invested or bet on the future direction of interest rates tied to LIBOR (the benchmark interest rate at which major global banks lend to one another) while being claimed to be rigged or known ahead of time so that the derivatives bets had a better chance of success.

Several publications like Rolling Stones Magazine wrote articles about the LIBOR Scandal potentially being the largest financial scandal in world history that affected upwards of $500 to $700 trillion in global assets. The named financial institutions in various publications or lawsuits which were alleged to have benefited, directly or indirectly, in the LIBOR Scandal included Deutsche Bank, HSBC, Barclays, Citigroup, JP Morgan Chase, and the Royal Bank of Scotland.

What’s important to understand is that many of the best known banks in the world may only have a few trillion of depositor assets in their checking and savings accounts today. However, they may have exposure to upwards of $50 + trillion in derivatives. As a result of their financial exposure to derivatives, these banks may be unwilling or unable to make investment property loans to even their most creditworthy clients partly due to tighter lending restrictions that came from the passage of the Dodd-Frank Act back in 2010.

This is why mortgage brokers and their non-bank lending partners became the better funding solution for investors while “handshake deals” at local banks don’t matter as much because so many banks may be technically insolvent.

Ironically, it was claimed that delinquent subprime mortgages represented less than 1% of all financial losses related to the Credit Crisis or Financial Crisis. Rather, the complex derivatives investments that were leveraged 50+ times the original amount of investments such as interest-rate options were the root cause. Sadly, mortgage professionals and stated income subprime loans still continue to be primary scapegoats. As a result, fewer banks are willing to offer more flexible residential or commercial property loans that don’t verify income.

Value Analysis for Commercial Properties

How lenders analyze income and expenses for commercial properties can be quite complex and overwhelming. Properties that do not meet most or all of these stringent underwriting guidelines may be prime candidates for asset-based loans.

Let’s try to review and simplify some key valuation terms that lenders may consider before approving or denying a borrower’s request:

Loan-to-value (LTV): The proposed loan amount as a percentage of the estimated property value. Many lenders prefer a loan-to-value range somewhere within the 50% to 75% LTV range. For purchase deals, these same lenders prefer that their clients put upwards of 25% to 50% of the purchase price as a cash down payment, depending upon the creditworthiness of the borrower and the property type.

Net Operating Income (NOI): The NOI for a commercial property can be summed up as follows: Gross Income – Operating Expenses = NOI

The property’s operating expenses include insurance, property management, utilities, and other day-to-day costs related to maintaining the property. However, the mortgage payments are not included within the NOI calculation.

Cap or Capitalization Rate: It’s a mathematical formula used to calculate the real or projected future rate of return on a property based on the net operating income that the property generates. The lower the cap rate, the better the property. Higher cap rates, in turn, are viewed as riskier investments. Cap Rate = NOI / Current Market Value

Property values and cap rates are inverse to one another like a seesaw. Decreasing cap rates as seen with prime downtown properties that are fully occupied leads to increasing property values. Conversely, rising cap rates for older rundown commercial properties usually correspond with falling property values.

Value Estimate: The property’s value estimate can be determined by way of the following formula: NOI / Cap Rate

For example, let’s look at two multifamily apartment buildings located in different cities with the exact same NOI but cap rates that are not nearly the same:

Building 1: $160,000 NOI divided by an 8% cap rate ($160,000 / .08%) = $2,000,000 value

Building 2: $160,000 NOI divided by a 4.5% cap rate ($160,000 / .045%) = $3,555,556 value

Generally, multifamily apartment rates have the lowest cap rates for income-producing properties that aren’t considered to be residential (one-to-four unit) properties. As per an analysis for the 2nd quarter of 2022 by Real Capital Analytics and the NAR, here are their numbers:

Property Type Apartments Industrial Office Retail

Cap Rate 4.5% 5.7% 6.3% 6.3%

DSCR: The easiest way to remember the debt service coverage ratio (DSCR) is that it’s used to determine whether or not a property has positive (1.25x), neutral or break-even (1.0x), or negative cash flow (0.75x). The DSCR is the ratio of operating income that’s available on a monthly or annual basis to service or cover the monthly mortgage payment (principal, interest, property taxes, insurance, etc.). As a mathematical formula, the DSCR can be visualized as follows: NOI / Debt Service

A small retail center that generates $10,000 per month in operating income and has a projected $8,000 per month in total mortgage payments would be calculated at 1.25x DSCR because the monthly or annual cash flow is 25% higher than the debt service ($10,000 / $8,000 = 1.25x). The net difference between $10,000 inflow and $8,000 debt service outflow is $2,000. This can also be calculated as $2,000 divided by the $8,000 in debt service ($2,000 / $8,000) which equals 25% more net cash flow to arrive at 1.25x DSCR.

Debt Yield: The commercial property’s NOI as a percentage of their total loan amount. The mathematical formula is as follows: NOI / Loan Amount = Debt Yield

For example, a small industrial building owner collects $100,000 NOI each year. His existing mortgage loan balance is $1 million, so his annual debt yield is 10% ($100,000 NOI / $1 million mortgage balance).

Multiple Underwriting Approval Solutions

As you better learn how lenders analyze properties, you will clearly understand that you have more than one loan program available. Some properties and owners will easily qualify after sharing tax returns, liquid assets, profit-and-loss statements, and a detailed income and expense history for their property. Other investors, however, know that their property’s cash flow is break-even or negative, but the future upside for these properties can be tremendous after occupancy rates are pushed higher.

Many commercial property owners experienced unusually high vacancy rates in recent years due to the combination of the pandemic, skyrocketing inflation, rising tenant payment delinquencies, and increasing rates for consumer debt. If so, the income and expense numbers for these commercial properties will probably not qualify at a traditional bank.

Commercial borrowers are more likely to qualify with asset-based nonbank lenders that may not closely review the income and expense numbers for the property. The verifying of income for asset-based, nonbank lenders isn’t necessary because these loans are based more on the appraised value of the subject property and its future income potential. At a later date when the income and occupancy rates are higher while the operating expenses decline, the owner can refinance into a much longer loan term at a lower rate and monthly payment.

Remember, it’s much better to have multiple lending options available for your property purchases or ballooning loan or cash-out refinance needs than just one local bank. The more efficient and flexible the mortgage broker’s technological systems and nonbank lending sources, the more likely you will close your loan and create significant income and increased wealth.

Rick Tobin

Rick Tobin has a diversified background in both the real estate and securities fields for the past 30+ years. He has held seven (7) different real estate and securities brokerage licenses to date, and is a graduate of the University of Southern California. Rick has an extensive background in the financing of residential and commercial properties around the U.S with debt, equity, and mezzanine money. His funding sources have included banks, life insurance companies, REITs (Real Estate Investment Trusts), equity funds, and foreign money sources. You can visit Rick Tobin at RealLoans.com for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/10/mortgage.jpg3901000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-10-05 04:37:402022-10-05 04:37:44Simplifying and Automating Commercial Mortgages

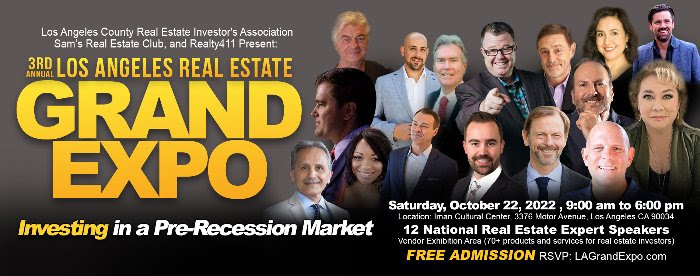

We are excited to announce our 3rd Annual Los Angeles Real Estate Grand Expo. The Grand Expo returns on Saturday, October 22, 2022, 9:00 am to 6:00 pm. The theme of this year’s Grand Expo is “How to Invest in a Pre-Recession Market.”

Last year, the Grand Expo was the largest real estate event in Southern California. We had over 700 investors, 64 vendors, and 10 national speakers. This year’s expo will be even BIGGER! We will spend an entire day celebrating real estate investing and how you can be involved. Best of all, the Grand Expo will be FREE to attend.

SPEAKERS. There will be national guest speakers (in three breakout rooms). Here is a partial list of speakers:*

1. Brent Kessler

2. Rusty Tweed

3. Shawn Tiberio

4. David Tedder

5. Merrill Chandler

6. Cliff Gager

7. Joe Arias

8. Tony Watson

9. Abbas M. (Featured)

10. Rick Sharga (Keynote)

INVESTMENT EDUCATION. Just think of it! An all-day in-depth educational extravaganza celebrating real estate investing. More importantly, this will NOT be a sales pitch. Each of the speakers have contractually agreed to educate and teach us successful real estate investing strategies. So regardless of whether you are a new investor, already own properties, or are very experienced, our Grand Expo is for you!

COMPLIMENTARY PRIVATE CONSULTATIONS. As a special unique feature of our Grand Expo, you can sign-up for private half-hour consultations with your favorite guest speakers. Registration will occur Saturday morning, starting promptly at 8:00 am. First come – first serve. So come early and schedule your private consultations. A once in a lifetime opportunity to get free advice from national real estate experts!

VENDOR EXPO: Don’t miss our “Vendor Expo,” which will occur throughout the day in the North Hall. We’ll have 60+ vendors where you can “meet and greet” real estate professionals with services and products that you’ll want to utilize in your real estate investing. (If you have a product or service that would be valuable to real estate investors and would like to be a vendor, please contact us directly.)

DATE: Saturday, October 22, 2022

TIME: 9:00 am to 6:00 pm.

LOCATION: Iman Cultural Center, 3376 Motor Avenue (between Palms and National), Los Angeles, 90034.

FREE PARKING: There will be plenty of street parking (metered and free) on side streets around the venue. Plus valet parking ($15) will also be available.

FREE ADMISSION: Admission to our Grand Expo will be COMPLIMENTARY, but guests must register in advance.

PRODUCERS. The Grand Expo is a joint presentation of the Los Angeles County Real Estate Investors Association, Sam’s Real Estate Club, Ventura Real Estate Investors Association, Realty411.com and REI Wealth magazine.

* Speaker schedule subject to change without notice..

For up-to-the minute updates, be sure to follow us on social media:

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/10/expo.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-10-03 07:08:512023-02-08 02:44:56Gain a Competitive Edge at the Los Angeles GRAND Expo.

You’re Invited – New Webinar: Learn Why the Future of 1031 Exchanges are Managed

Join us for our newest webinar and get educated on 1031 Exchanges to make better real estate investment decisions.

TOPIC:The Future of 1031 Exchanges: Top Concerns to be Aware Of (such as: timing, tax impact, cash flow, estate planning, passive vs. active, replacement asset availability, etc.).

This exclusive webinar will dive deep on the following:

Traditional retail assets: (active management, local buildings) VS. Institutional thesis (diversification across asset classes, ideal geographies, etc.)

Real Estate / Real Property asset classes: Land Banking, Infrastructure Development, Single Family Housing (SFH), Multifamily Housing (MFH) apartment communities, Hospitality (Hotels, etc.)

Addressing Each Concern: timing/tax/exchange execution

THIS EXCLUSIVE WEBINAR IS LIMITED TO THE FIRST 500 INVESTORS WHO REGISTER.

About Our Educator: Joel M. Desilets is the President of the Damascus Partners family office. The Desilets family supports causes through The Desilets Philanthropies Fund. Giving is done as a family activity that reflects the diverse philanthropic interests of Desilets family members.

A highly disciplined business leader and Real Estate expert with over 20 years of experience investing and managing throughout the U.S. as a General Partner (GP) in over 6,000 Multifamily apartment units, he has expertise in private wealth encompassing land banking and infrastructure development, single-family home building, investment in venture capital, hedge funds, and multi-strategy private equity, hotels, and other hospitality developments.

For up-to-the minute updates, be sure to follow us on social media:

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/10/webinar.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-10-03 05:02:142022-10-03 05:58:26Join Us for a New Webinar about 1031 Exchanges

We are certainly in exciting times for real estate investing. A lot may feel like it is changing from our 12-year bull run. But if you’ve been through a cycle or two in the past, then this may feel a lot more familiar and predictable.

Success in the months and years ahead is going to largely depend on investors’ financial position and access to capital.

Critical questions all investors should be asking themselves right now include: If their debt has been optimized to survive, what’s next? And, will they be able to secure new funding to keep thriving and growing as more opportunities arise?

Meet Joe

We caught up with Joseph V. Scorese to gain insight on the lending landscape, including what we can expect from lenders and what types of funding is still available for investors.

Joe is Regional Development Manager, Northeast, for Lending One. A national private lender focused on providing loans for real estate investors, LendingOne has funded over $1B in loans.

He has personally been investing in this space since 1992. So, he certainly knows a thing or two about the market, how it works and how to make the most of it.

One of the things that Joseph is most passionate about is educating others on the availability of private money and how it can be used to grow their real estate investing.

ADVERTISEMENT

What Exactly Are Private Real Estate Lenders?

Joseph specifically wants investors to understand that there are alternatives to the credit sources that they used to be limited to.

In his opinion, traditional banks and mortgage lenders really let investors down in the wake of the Great Recession. He doesn’t see them stepping up to be competitive or provide the backing that real estate investors need now or will need in the next phase.

At the other end of the mortgage market spectrum have been hard-money lenders. They have certainly had their place in the market, although their high-interest rates and limited scope of underwriting hasn’t made them the optimal solution for many.

Today, LendingOne is a private real-estate lender. A distinctly different industry to the others. LendingOne is backed by Blackstone and its deep pockets of private capital.

They are an asset-based lender. Though in contrast to hard money, they also look at DSCR (Debt Service Coverage Ratio), plus the strength of the borrower and their experience. This allows them to make more aggressive loans — with better rates and terms than hard money lenders — while providing loans that traditional mortgage lenders wouldn’t consider due to their rigid underwriting criteria.

ADVERTISEMENT

The Current & Evolving Landscape

We picked Joe’s brain for his insights on the current market and what’s ahead.

While no one knows exactly how things will play out, with enduring inflation — the highest in 40 years — he acknowledges that we could probably use some cooling in the housing market. Not that we need a crash, but more sustainable growth would be wise.

We have already seen a significant reset in the past 90 days. Joe says that in addition to the extra inventory we’ve seen coming along over the past couple of months, there are a lot of foreclosures in the works. It could be another 12 or 18 months before they hit the market. Together these factors suggest that there is going to be a lot more negotiability for acquisitions coming and hopefully more discounts to be found.

So far the only obvious changes in the lending space have been in interest rates. Most of today’s investors weren’t around when rates were at 20% or even 14%. Joe says that while they might not get that high, they are indeed rising. He predicts they will likely hit the 8% to 9% range.

This should definitely be creating a sense of urgency among investors to do two things:

Optimize current debt structures to make it through this phase of the market.

Lock in great long-term fixed rates on new acquisitions while rates are low.

Additionally, investors need to be really getting in tune with their numbers, evaluating their assumptions and bids, and planning for new dynamics in the market.

Loan Programs To Fuel Your REI Business

Joseph V. Scorese says that LendingOne has $3B already committed to lend next year. He expects that to be consistent over the next several years.

LendingOne offers a variety of real estate financing options, including the following.

Fix & Flip Loans

Up to 90% of purchase and repair costs, and closing in as little as one week. BRRR-friendly, and interest-only payment options.

Rental Property Loans

Loans for individual rental properties, with 30-year fixed-rate options, no personal tax returns needed, and corporate borrowers allowed.

New Construction Loans

Ground-up construction loans with interest-only payments for up to 24 months.

Multifamily Property Loans

Multifamily bridge loans for value-add apartment building projects with loan amounts up to $15M, and no DSCR requirement at closing.

Portfolio Rental Loans & Blanket Mortgages

These loans are ideal for those with five or more rental units, with 30-year fixed-rate loans, and loan amounts up to $50M.

Smart Money Moves To Make Now

With the insights we gained from Joseph in our interview, it seems there are some obvious moves most investors should be making.

Recalibrate your buying criteria to demand better deals

Refinance now avoid rate shock on loans maturing in the next couple of years

Lock in long term fixed rate loan terms on new acquisitions now

Be sure you are staying on top of market changes on a daily basis

Find out more about LendingOne and their financing options at LendingOne.com.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/09/invest.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-09-23 06:24:412022-09-23 06:24:45How To Use Private Money To Secure & Grow Your Real Estate Investing

The number of NOD pre-foreclosures

notices are on the rise. Fortune magazine reports they are up triple digits in

2022 compared to 2021. There are several factors causing the uptick: COVID

mortgage forbearance overhang, the current recession, rapidly rising interest

rates this year, etc. The increase in the number of homeowners and landlords in

trouble is causing a lot of (both note and property) investors to start taking

a hard look at how they can profit from these changes in the market.

Precautions include:

ADVERTISEMENT

1. Depreciating prices. For those who came into the investor market after the last downturn, you may not be aware that residential property prices in many markets dropped by 40%, from peak (2008) to trough (2012). Some areas/types of real estate dropped by even more. The cautionary tale is to be sure to build in enough equity in foreclosure properties you seek to acquire. In an up market, where prices are appreciating double digits every year, how much equity you initially acquire is usually not the first box you check as an investor. However, as the old saying goes: That was then, and this is now. Assuming the recession worsens, you need to build in more of an “equity buffer” into each deal to protect yourself from making no profit (or actually losing money) when you go to sell the property or note.

2. Judicial vs. non-judicial states. The number of virtual wholesale note and property deals are increasing nationwide; wholesalers need to be knowledge about what laws apply in the state in which the investment is being made. About half the states in the nation are what is referred to as non-judicial. That means they typically employ what are known as trust deeds and trust deed notes. The foreclosure is undertaken without using lawyers and judges. Judicial states usually require you to go through the court system to adjudicate your claim. Non-judicial states usually cost less and take less time to foreclose.

3. Beware of Land Contracts (LCs). An LC is an agreement in which the owner/seller of a property agrees to act as the bank and personally finance the sale for the buyer instead of going through a 3rd party, such as a bank or credit union. The buyer makes monthly payments to the owner, but does NOT receive actual title to the property until the last payment is made; and the last one is often a “balloon” payment, i.e. for a very large amount (that the buyer perhaps cannot afford to make).

As an investor (of a property or a

note secured by a property) who is about to step into this breach, you must

give careful consideration to the LC contract that the owner has/had with the

LC buyer. What you want to avoid is getting subsequently sued by the buyer

after you bought out the interest of the seller.

ADVERTISEMENT

For example, does the seller own the

property outright, or is he still making payments to a lending institution? If

the owner himself did not make regular payments for any reason, the property

can be foreclosed upon, leaving the buyer with a worthless contract and no

home. Land contracts also leave the new owner (you) tied to the property. If

the buyer stops making their payments, you become responsible for the

land—which means you could lose the property altogether if the buyer fails to

insure it properly or pay their property taxes.

All of these tricky issues must be taken into account when you are considering an acquisition that includes a land contract. You need to have a very clear understanding of everyone’s rights and responsibilities beforehand. To play it safe, retain legal counsel to look everything over first.

4. Watch out for Super Liens in 20 states. There are approximately 370,000 homeowner associations (HOAs) in the United States. Collectively, this represents more than 40 million households (or about 53% of the owner-occupied households in America). Statistically, about 26% of all Americans live in HOA communities. Typical HOA/association dues & fees run from $200-$300 per month—many charge more, some charge a LOT more.

In most states, when a lender

forecloses on a property in a HOA, and the property owner has also defaulted on

their association fees, odds are the condo association won’t get paid for those

debts. That is because a successful foreclosure action by the holder of the

first position mortgage typically wipes out all junior notes and many liens.

However, in about 20 states (see the list below), “super lien” laws have been

passed that protect the association from being wiped out completely.

A foreclosure by a bank or credit

union can take many months. During that time the HOA is not receiving the

monthly payments due to them. When the bank finally forecloses and sells the

property, and surplus funds are left over, the HOA (in a Super Lien state) can

typically petition the court to channel that money to the association, assuming

the association has properly recorded a lien.

So, if you are a note or property

investor, be sure to check carefully if the state in which you are investing

(and where you could potentially foreclose on a property) is a super lien

state. If so, you need to take that information into account, and build those

costs into your bid price for the note or property.

To reiterate, about 20 states allow

for some form of super lien. Each of the states has differing laws when it

comes to how an HOA lien becomes a super lien. You can learn more about super

lien states and their individual laws regarding super liens by looking up your

state statutes which can usually be found online. The following states allow

for super liens, or some version of priority liens for community associations:

Alabama, Alaska, Colorado, Connecticut, Delaware, District of Columbia,

Florida, Hawaii, Illinois, Maryland, Massachusetts, Minnesota, Nevada, New

Hampshire, New Jersey, Pennsylvania, Rhode Island, Vermont, Washington, West

Virginia.

What We Do: Provide 100% Joint Venture Funding, nationwide, to real

estate note and property wholesalers. Contact info: Tod Snodgrass, [email protected],

310-408-7015

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

We are very excited to announce our 3rd Annual Los Angeles Real Estate Grand Expo. The Grand Expo returns on Saturday, October 22, 2022, 9:00 am to 6:00 pm. We’re taking over the entire Iman Cultural Center for the day – it’s all ours! The North Hall (vendor hall), the South Hall (workshops), and the middle parking lot (loaded with tents and food trucks). The theme of this year’s Grand Expo will be “How to Invest in a Pre-Recession Market.”

Last year, the Grand Expo was the largest real estate event in Southern California! We had over 600 investors, 64 vendors, and 10 national speakers! This year will be even BIGGER! An entire day celebrating real estate investing and you can be involved. Best of all, the Grand Expo will be FREE to attend. This Expo is going to be big, really BIG!

SPEAKERS. There will be national guest speakers (in three breakout rooms). Here is a partial list of speakers:

1. Brent Kessler

2. Rusty Tweed

3. Shawn Tiberio

4. David Tedder

5. Merrill Chandler

6. Cliff Gager

7. Joe Arias

8. Tony Watson

9. Abbas Mohammed

10. Rick Sharga (Keynote)

INVESTMENT EDUCATION. Just think of it! An all-day in-depth educational extravaganza celebrating real estate investing. More importantly, this will NOT be a sales pitch. Each of the speakers have contractually agreed to educate and teach us successful real estate investing strategies. So regardless of whether you are a new investor, already own properties, or are very experienced, our Grand Expo is for you!

COMPLIMENTARY PRIVATE CONSULTATIONS. As a special unique feature of our Grand Expo, you can sign-up for private half-hour consultations with your favorite guest speakers. Registration will occur Saturday morning, starting promptly at 8:00 am. First come – first serve. So come early and schedule your private consultations. A once in a lifetime opportunity to get free advice from national real estate experts!

VENDOR EXPO: Don’t miss our “Vendor Expo,” which will occur throughout the day in the North Hall. We’ll have 70+ vendors where you can “meet and greet” real estate professionals with services and products that you’ll want to utilize in your real estate investing. (If you have a product or service that would be valuable to real estate investors and would like to be a vendor, please contact us directly.)

DATE: Saturday, October 22, 2022

TIME: 9:00 am to 6:00 pm.

LOCATION: Iman Cultural Center, 3376 Motor Avenue (between Palms and National), Los Angeles, 90034.

FREE PARKING: There will be plenty of street parking (metered and free) on side streets around the Iman. Plus valet parking ($15) will also be available.

FREE ADMISSION: Admission to our Grand Expo will be COMPLIMENTARY (free!), but reservations are recommended.

RSVP: Make your reservations now! (Last year, we sold out and people were turned away at the Skirball!) So don’t wait! RSVP at our special website: www.LAGrandExpo.com.

PRODUCERS. The Grand Expo is joint presentation of the Los Angeles County Real Estate Investors Association, Sam’s Real Estate Club, Ventura Real Estate Investors Association, and Realty411.com.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/09/LAGrandExpobanner.jpg276700dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-09-14 05:45:052022-09-14 05:46:02You’re Invited to the 3rd Annual Los Angeles Real Estate Grand Expo

Attempting to curtail foreclosed houses being turned into rentals, California passed SB-1079 in 2021. This law effectively, for 45 days, suspended any activity after the foreclosure. Prior to this law, houses that were foreclosed on could be purchased at the foreclosure sale by investors and immediately turned into rental property. When this happened, houses were taken off the inventory for home ownership.

California was desiring to promote homeownership, and reduced inventory pushed prices higher as well as increased renters vs homeowners. The theory behind SB-1079 was that it would discourage investors from bidding at the foreclosure because, for the next 45 days, an “eligible bidder” could match the winning bid. The effect of this would be that the investor would tie up his money for 45 days and not know if he would end up with the property. Thus, investors would most likely not show up and bid at the foreclosure and wait out the 45 days to see if any eligible bidders came forward. If nobody outbid the lender at the foreclosure sale, the investor could approach the lender to purchase the property. With SB-1079 in place, there is no incentive for an investor to outbid at the auction.

ADVERTISEMENT

One of the main problems with this law is that the party being foreclosed on has almost no chance of any over-bidding at the foreclosure. Prior to SB-1079, it was possible for the borrower who was being foreclosed on to potentially recoup some equity in the property if the house was bid up. For example, if the 1st mortgage was owed $100,000 and was the foreclosing party, and the house was worth $300,000, the lender would most likely credit bid their entire $100,000 loan. If another party bid $140,000, the lender would get paid their $100,000 and the owner of the house who was getting foreclosed on would walk away with $40,000. SB-1079 effectively shuts the door on that scenario, as the chances of someone outbidding the lender at the foreclosure are slim due to the uncertainty of the bidder acquiring the property at the sale. For the following 45 days, an “eligible bidder” has the opportunity to bid the same $100,000 as the lender and end up with the property. Although there are eight definitions of an eligible bidder, the primary ones include an occupant of the property as his primary residence [not the borrower or a family member of the borrower, however], effectively, a rental, a prospective owner-occupant, and a California nonprofit whose primary activity is the development of affordable housing. If the house is owner occupied, that eliminates the potential tenant purchase option.

ADVERTISEMENT

The main problem is that the homeowner will almost certainly lose 100% of any potential equity due to nobody outbidding at the foreclosure auction. At this writing, there are not many non-profits who are set up for development of affordable housing; thus, the only realistic way for the lender to be taken out after 45 days [after the foreclosure] will be those houses that were rented out to tenants or those who desire to own and occupy the house as their primary residence. This last potential is slim, as most buyers want to make offers on houses they can inspect and not wait 45 days to find out whether or not they will be allowed to buy the house.

Due to these new foreclosure laws in California, lenders will have to factor into their underwriting the potential added costs of holding a [potential] foreclosed property at the time they make their loan to the borrower, as the lender is precluded from selling or renting out the property for 45 days after the foreclosure. The lender may have additional costs during this period, such as securing the property against vandalism, vagrants, weed abatement, and the like.

It is still too early to tell if the statistics show if tenants come up with the needed funding options in order to secure the house for their own benefit, as the program is still in its infancy. Only time will tell if this experiment works out for potential would-be homeowners or if it was just a sure-fire way to make sure foreclosed homeowners recoup nothing.

ABOUT EDWARD BROWN

Edward Brown currently hosts two radio shows, The Best of Investing and Sports Econ 101. He is also in the Investor Relations department for Pacific Private Money, a private real estate lending company.

Additionally, Edward has published many articles in various financial magazines as well as been an expert on CNN, in addition to appearing as an expert witness and consultant in cases involving investments and analysis of financial statements and tax returns.

Edward Brown, Host The Best of Investing on KTRB 860AM The Answer on Saturdays at 8pm and Sports Econ 101 on Saturdays at 1pm on SiriusXM channel 217 21 Pepper Way San Rafael, CA 94901 [email protected]

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/09/foreclosure-troubles.jpg4721080dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-09-13 02:58:302022-09-13 02:58:32The Reality of SB-1079 Foreclosures